14. HoldCo Debt Financing Structures

Structuring back leverage to reduce equity contribution and/or effectuate a dividend

First off, thank you for subscribing and engaging with the page. It is much appreciated and hopefully indicative of your interest in these topics!

We have previously discussed cascading ownership in posts 5, 6 and 7. I would start with those before reading this post.

In those discussions, for simplicity, we ignored the impact of leverage in understanding the equity and distribution dynamics. On the equity side, the goal is the maintain control while minimizing the equity need from the sponsor. On distributions, the goal is to structure priority of distributions / build a favorable waterfall.

We saw that many mechanisms exists to accomplish these goals: cascading, different share classes, voting shares, distribution preferences, promote, etc. All of this was understood in a scenario in which the equity and distributions are free from covenant restrictions.

Now, let’s begin to layer in debt financing at the various levels. Specifically, HoldCo and OpCo debt financing.

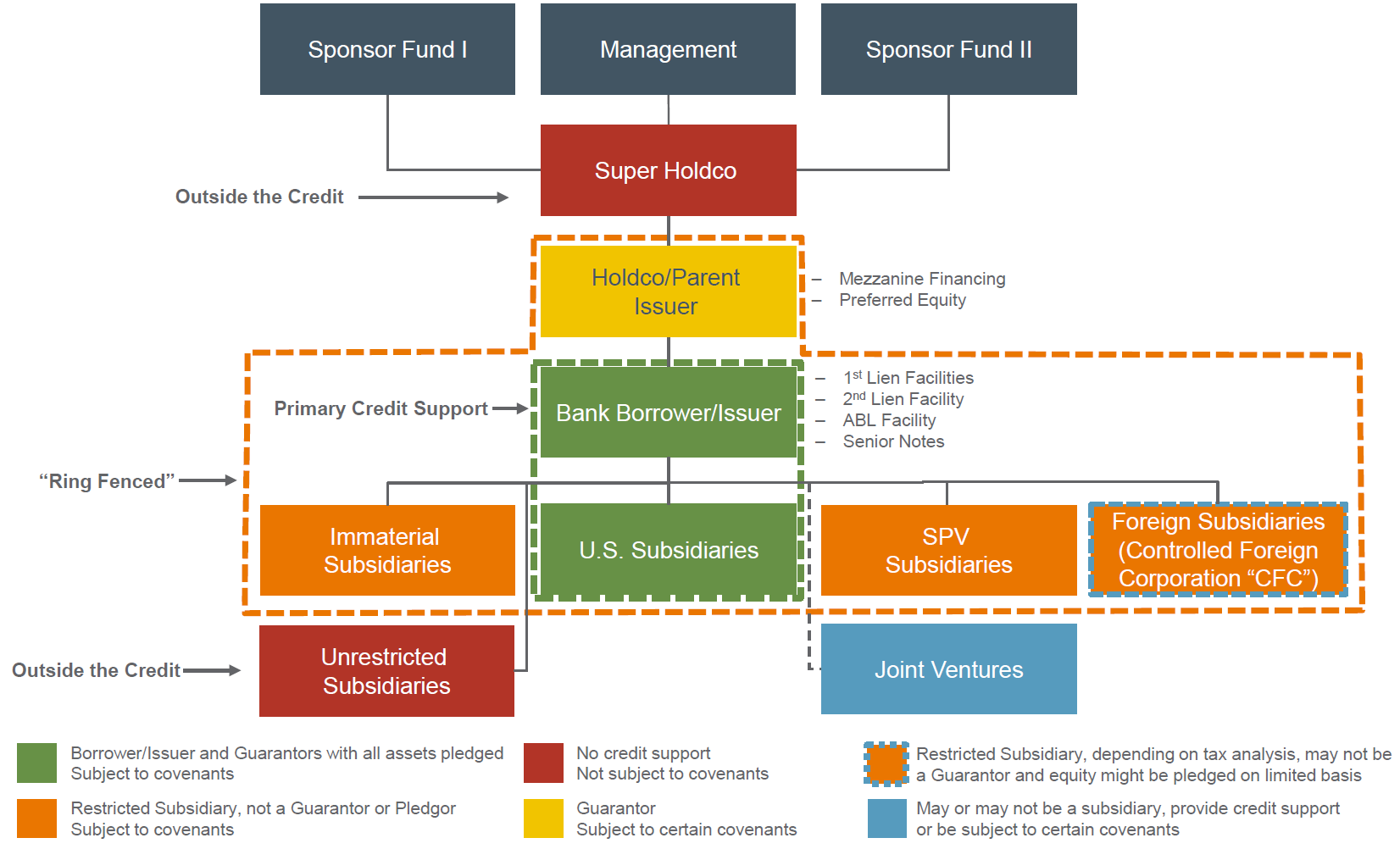

HoldCo Financing / Back Leverage

Holding companies (HoldCo) sit above operating companies (OpCo). Various levels of debt usually exist at the OpCo level - revolver, senior loans, secured notes, unsecured notes, etc. All of this debt forms the credit group. Remember that any OpCo debt is structurally senior to HoldCo debt. Also, in our case, we are assuming debt comes in at Super Holdco (so, above the credit group).

Historically, HoldCo financing has been popular in infrastructure and energy sectors in which companies provide a steady, predictable stream of cash flow to service the HoldCo leverage (strong and consistent cash flow at the OpCo level can be sent to the HoldCo via a distribution assuming plenty of restricted payment, RP, capacity). Post 9, linked above and here, talks about RP capacity in more detail.

The HoldCo lenders are typically different from those who provide senior debt to OpCo. However, some senior debt OpCo lenders may choose to provide the HoldCo financing (this is the case for Citicorp and Robert Campeau in the 80s. I’m working through a post on Campeau’s famous LBO of Allied and Federated…more to come).

Key Features

One way to think about HoldCo leverage is that it lets you increase leverage of the broader group (HoldCo and OpCo) without impacting the OpCo’s leverage stats.

For instance, let’s say OpCo debt is capped at 4.0x and is currently fully levered to 4.0x. So, no more debt may be incurred at OpCo as governed by the covenants.

But, HoldCo debt sits beyond the confines of the OpCo credit agreement. Debt incurred at the HoldCo level will not increase the OpCo leverage above 4.0x (although the broader group’s leverage will in fact increase beyond 4.0x).

HoldCo leverage is usually put in place for one of the following:

to finance an investment in the OpCo

to finance an investment of assets outside of the OpCo group

to make a distribution to the sponsor / shareholders of the HoldCo

Often in situations where the ability to make distributions at OpCo is limited by the credit agreement covenants

Let’s pause on point 3. This is very helpful in a scenario where the sponsor wants to take a distribution but the OpCo covenants prevent such a distribution from being taken out of the credit group. Instead, the sponsor can align HoldCo financing to effectively execute a dividend recap.

Another common use of HoldCo debt is to reduce the initial sponsor equity need when acquiring a new asset. This is common in the world of infrastructure buyouts and minority stake deals.

It’s worth noting that there are situations where the HoldCo debt may be included in the OpCo credit group and therefore limits flexibility of using HoldCo debt proceeds for a dividend.

A few other key terms include:

HoldCo debt maturity date outside of the OpCo senior debt maturity

Flexible interest provisions ranging from cash, cash + PIK, to full PIK

Full PIK is the most aggressive structure and was referred to as cramdown paper in Campeau’s case

Principal repayments can be made as a bullet payment on maturity

Naturally, the terms will vary by deal. Some may be cash interest while others PIK. Some may have aggressive amort schedules while others allow for a bullet repayment. Etc., Etc.

Other Key Notes

Remember that the HoldCo debt is structurally subordinate to OpCo debt. Further, HoldCo collateral is often limited. Lenders may take security over the HoldCo equity shares, but the enforcement of such collateral would likely trigger a change of control (CoC) defined by the OpCo’s credit agreement. A CoC would often force mandatory prepayment of the senior OpCo debt.

If the OpCo does not have sufficient assets to repay the senior debt in this scenario, the HoldCo equity interest would be of little value (this will come up when I get the Robert Campeau post out!).

So, think about this from the HoldCo lender’s perspective. Your collateral (often the HoldCo equity interest) is limited if the OpCo asset value erodes. What else might concern you?

The distributions from OpCo.

First, OpCo needs to generate sufficient cash to have excess funds available for distribution. That’s one major point to diligence (i.e. get comfortable with the underlying business and cash generation).

Secondly, there needs to be enough RP capacity to get those distributions out of OpCo to the HoldCo.

HoldCo lenders and the sponsor should 1) be comfortable with the underlying business and 2) understand any distribution restrictions governed by the OpCo credit agreement.

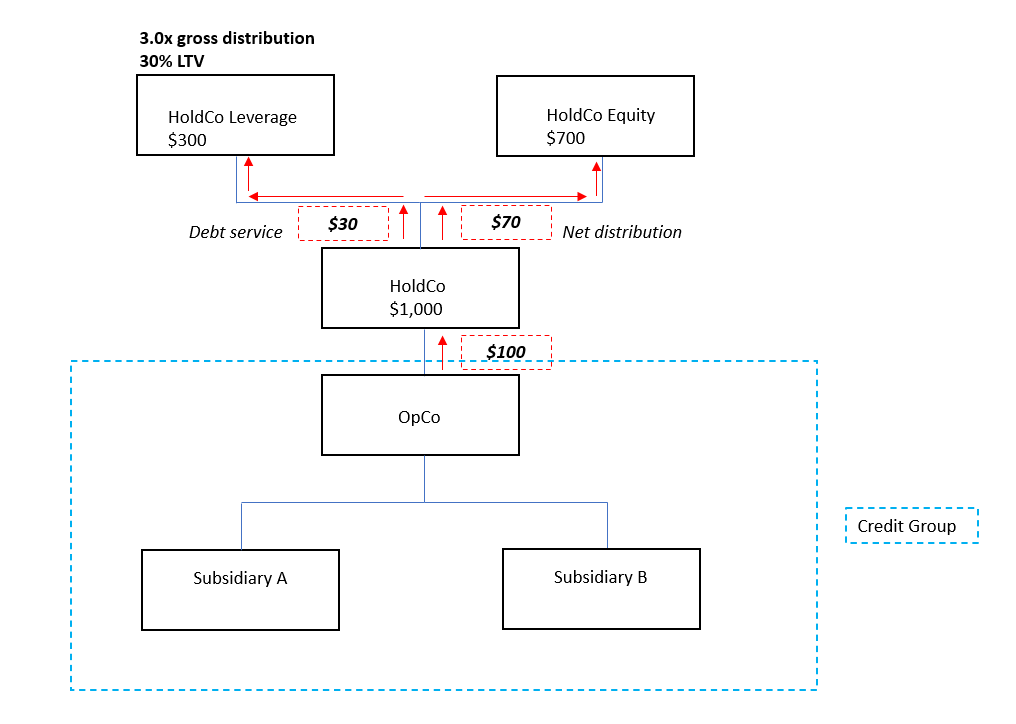

Shifting gears, to size the HoldCo, you look at 1) LTV and 2) a multiple of distributions. You may see HoldCo loan sizes in the range of 30-40% LTV and 3.0x - 4.0x gross distributions.

Also, think about the cash items at HoldCo. Let’s say $100mm is sent to HoldCo from the OpCo. This is $100 gross distribution, which is how the leverage statistic is calculated. 3.0x this amount would indicate a $300mm HoldCo loan. OK, that works.

Other assumptions: $300mm HoldCo loan, 1% amort, 9.000% fixed cash interest (for simplicity, let’s assume fixed and not floating rate. Note the debt can be structured as a term loan A, term loan B, secured/unsecured note, etc.).

So, in year 1, your HoldCo leverage is 3.0x gross distributions. Then, take out the $3mm of amort and $27mm of interest ($30mm debt service) to get $70mm of net distributions. Excluding any taxes at HoldCo, the net distributions can be thought of as the HoldCo free cash flow… ready to be sent to the sponsor via a dividend.

You can then take the $70mm out of the HoldCo (assuming no restrictions governed by the HoldCo lenders for simplicity). Dividend the $70mm to the sponsor. And you can model this out every year where you dividend out the gross distribution less debt service.

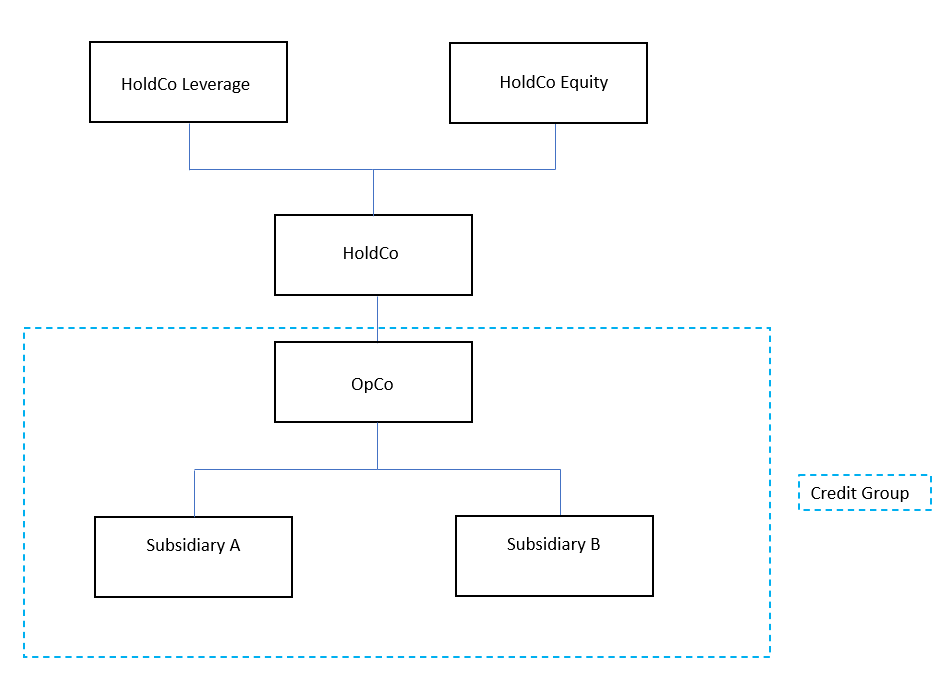

Here’s a sample structure:

Now we can layer in additional points:

I didn’t label this, but remember the $100mm is gross distribution.

And illustrating the key points around the $100mm distribution:

Conclusion

HoldCo financing accomplishes many different objectives for the sponsor.

1) Allows the sponsor to reduce the required equity on day 1 by borrowing against the HoldCo. This is further beneficial as it often will not increase the leverage ratio of the OpCo as it sits beyond the credit group.

2) HoldCo leverage may also allow the sponsor to take a dividend by incurring debt later in the ownership period.

3) HoldCo leverage does not further tighten or burden OpCo flexibility beyond what’s restricted via the senior debt credit agreement.

From various perspectives, whether you’re an OpCo lender, HoldCo lender, sponsor, etc., it is important to understand who sits above you in the capital structure. Who has seniority to the collateral and priority of distributions? What happens to your collateral in a worst case scenario? Are there overlapping liens on the collateral? What’s the equity value behind all of the leverage?

There are many angles to consider when constructing these structures. As we will see next, Robert Campeau built a house of cards with little equity contribution. Most of his “equity” was in the form of back leverage as illustrated above. Unfortunately, his levered house came crashing down.

He bet the ranch twice… and lost.

++

Until next time.

John Galt