5. Leveraged Buyouts to Cascading Ownership Structures (Part 1/3)

5. Leveraged Buyouts to Cascading Ownership Structures (Part 1/3)

LBO Financing, Oaktree's New $10bn Fund, Cascading Ownership

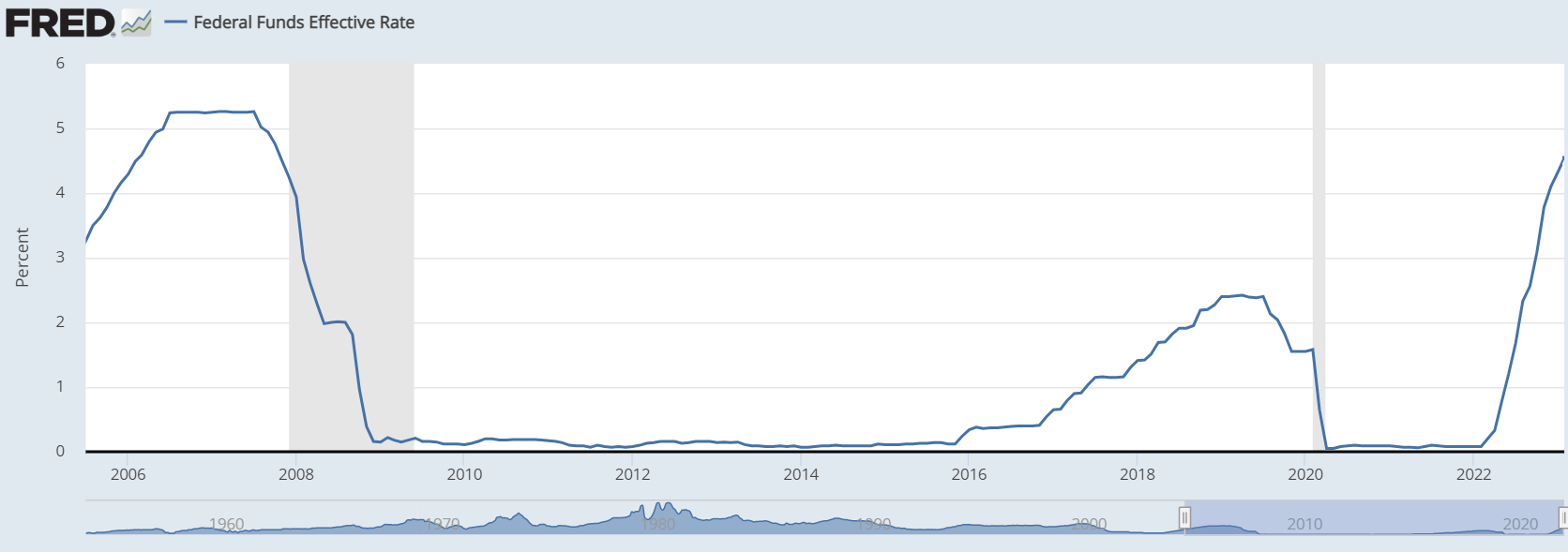

In March of 2023, financing for new LBOs remains abysmal. Both supply and demand dynamics are out-of-whack compared to the boom of 2021.

One driver is the Fed raising interest rates ~500bps, thereby dramatically increasing the cost of debt financing.

Further, as interest rates rise, there tends to be less demand to reach out on the yield curve by investing in high-risk assets (because you can sit on the short, safe end of the curve and earn an attractive yield). This is why you often see technology and VC sell-off first as rates rise.

Investor preferences shift toward parking money in an instrument that earns ~4% rather than an illiquid tech startup that won’t cash flow for 10+ years.

Back to LBO financing directly. Historically, sponsors (“GPs” | example: Blackstone) will go to a bank ahead of signing up a new LBO deal. For instance, let’s say Blackstone is looking to acquire a business where final round bids are due in 3 weeks.

Blackstone will go to the banks requesting a financing package before the bid date. Specifically, they look for commitment papers which can strengthen their bid to the seller (they get to say “hey look! I have the money!)

Often times these financing packages will combine a mix of new revolver, new term loan and/or new bonds.

So, as interest rates increase, this entire financing package becomes more expensive to Blackstone. AND, if sellers do not downwardly adjust their prices, then Blackstone eats the difference when thinking about returns.

Expanding on the last point: an increase in interest rates makes debt financing more expensive. Also, private markets valuations tend to react more slowly than public markets. So, in this period where rates are higher but valuations remain flat, the deals make far less sense from a return perspective.

That’s the demand side in a nutshell.

On the supply side, let’s shift to the banks. Historically, banks pucker up when providing LBO financing. It’s a lucrative business for them when looking a the financing fees and M&A assignments they receive. Oftentimes, banks who provide financing may receive buyside M&A titles or tips.

In 2022, banks came into the year with massive LBO commitments on their books. Citrix, Tenneco, Twitter to name a few.

Meaning, banks had already committed to terms at which they can deliver the debt financing. But, as interest rates rise and the market moves away from these terms, the banks are left hung out to dry.

Within the packages exist what’s called flex. This provides marginal cushion to the banks in the event the market moves and they need to flex terms to get the deal done.

However, in 2022, the market moved well outside of the flex on these deals. As a result, any loss beyond the flex eats into the transaction fee of each bank before hitting as an actual loss for the bank.

Flex —> fees —> loss

The market moved most of these deals into the loss territory for each bank.

So, each bank got burned… massively.

This leaves them unwilling to sign up new deals with such uncertainty about rates and future market appetitive. This is the big supply side issue.

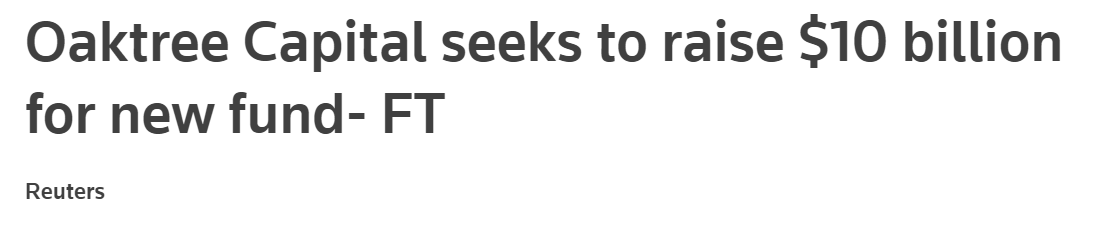

Oaktree - A New Player

On February 28th, 2023, Oaktree announced the expectation of raising $10bn for a new fund that would provide LBO financing to sponsors. Effectively, side stepping the banks much like other direct lenders have done for years.

Here’s what Oaktree said on their website:

Oaktree believes this market is especially attractive now, given the limited availability of debt capital to finance large leveraged buyouts (LBOs) and the record-high levels of committed private equity capital yet to be deployed, requiring financing. In Oaktree’s view, this imbalance has been driven by (a) the retreat of banks from this form of lending and (b) the constrained capacity of nonbank lenders that are fully invested and/or managing issues with prior investments.

This is very interesting, especially how they are coming in with a clean slate and can more eagerly capture the now high-yielding LBO loans.

Yields on large LBO loans have increased significantly in the last year, averaging 12.4% at year-end. This is primarily due to the dramatic spike in base rates during 2022 and the shortage of funding for large LBOs as described above. The companies that are the subject of these transactions often have critical mass and established track records, positioning them well to weather economic cycles. Thus, Oaktree believes the risk-adjusted return potential available in this segment of the market is currently more compelling than that of other more liquid asset classes and some other areas of private debt.

It’ll be interesting to see how direct lenders compete with banks moving forward. Banks largely seem shut to new LBO financing and time will tell if this appetitive comes back with the market.

Cascading Ownership

I’ve long understood that corporate ownership structures can be incredibly complicated. Tracing entities, who owns what, who has voting control and economic interests, etc., can be challenging.

Take The Frere Group as an example (December 2008… so it’s dated…and blurry! I guess that comes with age).

Another common example is LVMH.

Back to Frere, the Frere family controls 20% of Lafarge, but the family’s financial interest is only 1.5%. This is an example of how you can cascade ownership structure to maximize control while minimizing the required equity investment.

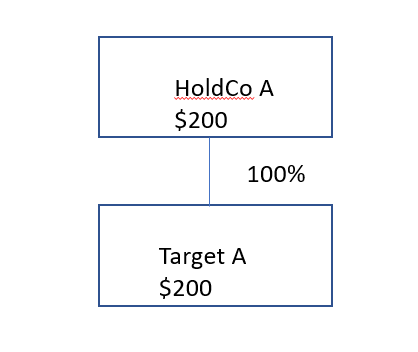

Let’s look at a very simplified example. Note that we are excluding the nuances of this structure for now.

We will look at various ownership structures in which the buyer acquires a new OpCo (known as Target A).

Below is the simplest example. HoldCo A finances 100% of the required equity and maintains 100% control over Target A.

HoldCo A: Source of funds…you…in this case, the owner, proprietor, family, etc.

Target A: Use of funds… an acquisition in this case.

The issue with the above structure is that it requires a large capital outlay from HoldCo to finance the full equity check. How can you reduce the required equity but maintain control?

Raise outside capital.

Investor A: new capital that you, HoldCo A, raise from outside investors.

Ok, wonderful. We just saw how HoldCo can maintain majority control while reducing the required equity check to finance the deal. Great!

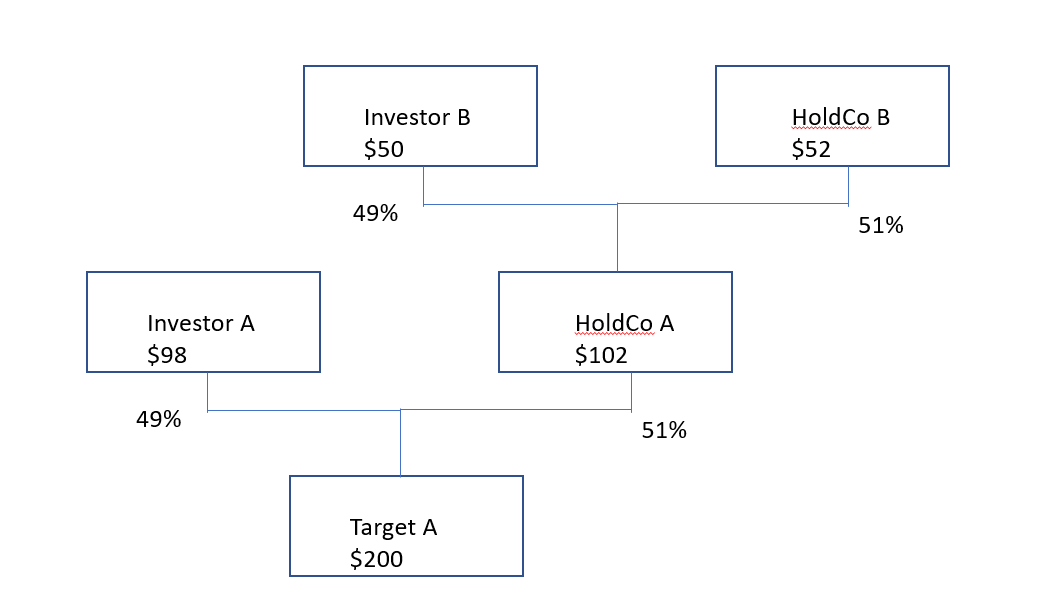

Let’s take it a step further… let’s cascade!

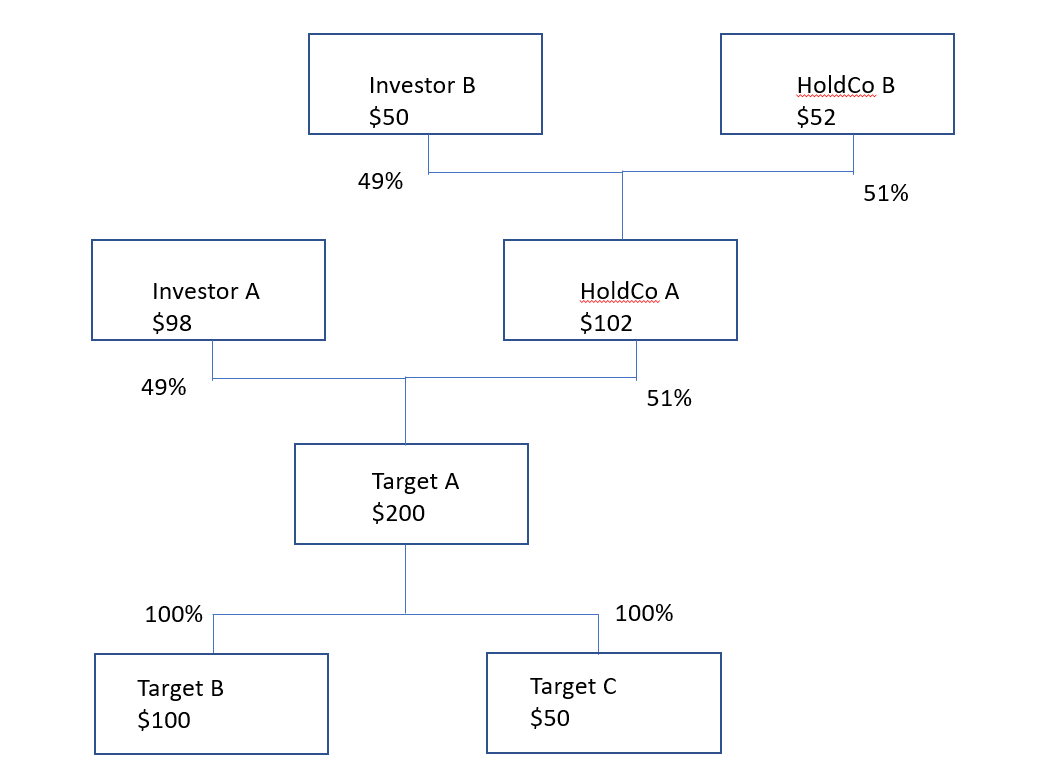

Now, we’re putting financing behind HoldCo A. For simplicity, we are assuming this is all equity financing. Let’s ignore leverage / back leverage for now.

To further reduce the capital that you must commit to finance Target A, you bring in Investor B as a minority interest of HoldCo A. Your equity commitment is now in the form of HoldCo B ($52 from $200 originally).

We can continue to unfold the Russian dolls and reveal additional layers. HoldCo C, HoldCo D, etc.

Or…. this also works at the Target level. Any subsidiaries that Target A acquires will inadvertently be controlled by HoldCo B.

Targets B and C are both, ultimately, controlled by HoldCo B! And all of this is with $52mm of capital contribution from HoldCo B. You can see how this dominos.

Ok, last fun example. You can bring outside investors directly into Target C to reduce Target A’s equity contribution in buying Target C. Looks like the below:

Let me pause.

I know this is an overly simplified illustration of the ownership structure. There are limitations in reality which I’m not addressing. There are further considerations beyond the scope of this discussion. For one, the further an asset sits from you (HoldCo B), the more difficult it will be to extract distributions. That is because dividends will leak to many different parties along the way.

Imagine sending a dividend from Target C to HoldCo B. Along the way, Investor C, Investor A, and Investor B all require their pro rata share. This erodes the ultimate distribution to you at HoldCo B.

But, the point of this discussion is to illustrate how organizations can be structured to retain control while minimizing the capital commitment.

Cascading ownership is your answer.

++

Until next time.

John Galt