7. A Quick Look at LVMH Ownership (Cascading Part 3/3)

7. A Quick Look at LVMH Ownership (Cascading Part 3/3)

Organizational Structure and Double Voting Shares

Let’s continue expanding on ownership structures, specifically those that allow the founder or family to maintain control through structuring means.

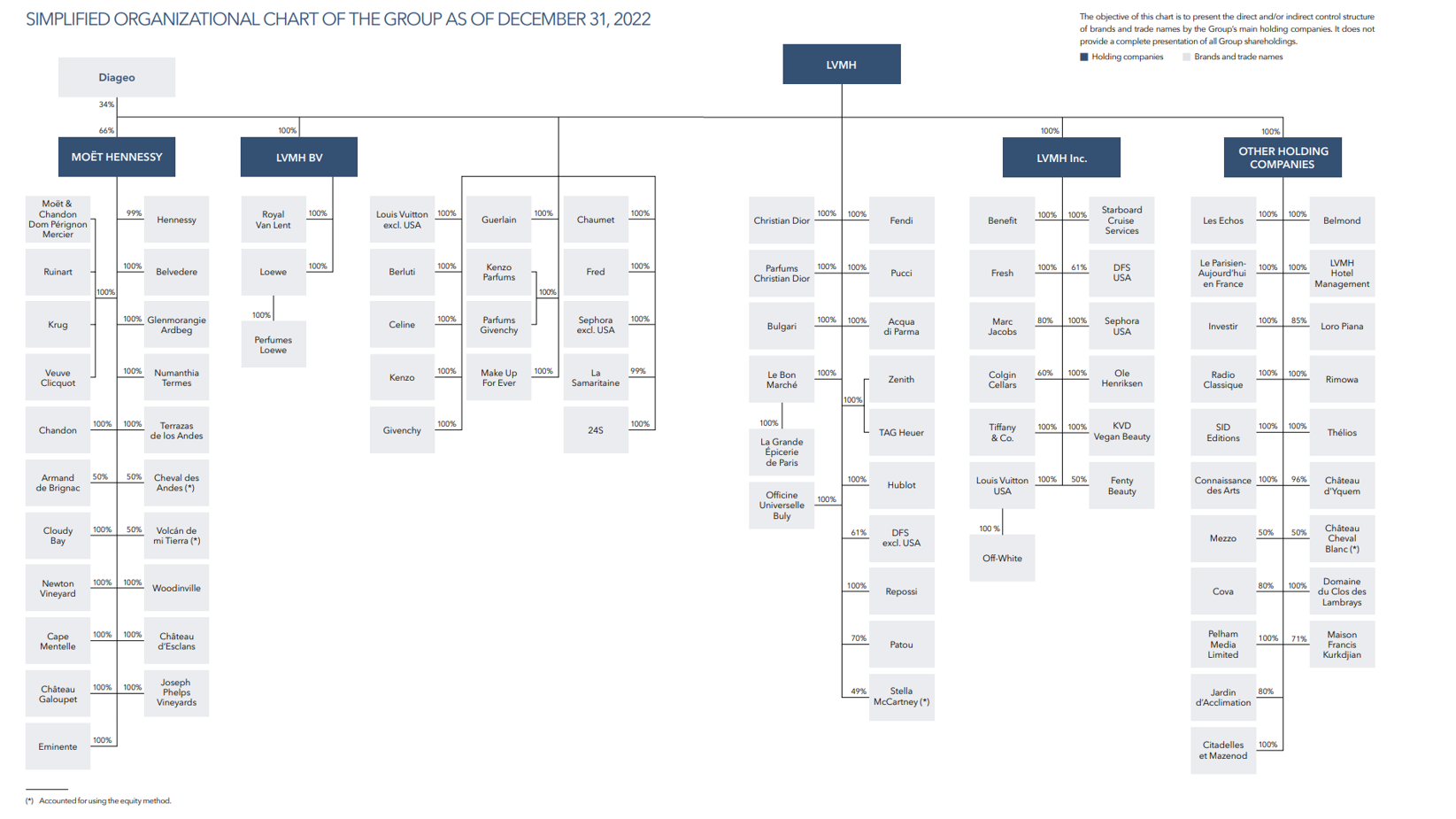

Below is the organizational structure of LVMH per the 2022 Universal Registration Document posted in March 2023.

Notice a few things:

LVMH holds a majority control of each holding company and most brand / trade names (excluding Stella McCartney which is accounted for using the equity method. Maybe Arnault holds a majority through a different entity. Or maybe the equity method pushes this percentage below 50% at times?). In most cases, LVMH holds 100% control of each brand. In others situations, which are few, LVMH may hold less control directly like DFS (60%), Fenty Beauty (50%) or Maison Francis (71%).

Diageo, a British multinational alcoholic beverage company, owns 34% of Moet Hennessy directly. I don’t know the history of this partnership, but maybe Arnault brought them in to raise cash for a different venture or to reduce his capital commitment in Moet.

The LVMH subsidiary structure appears fairly simple… but what if we pull back the curtain on LVMH ownership?

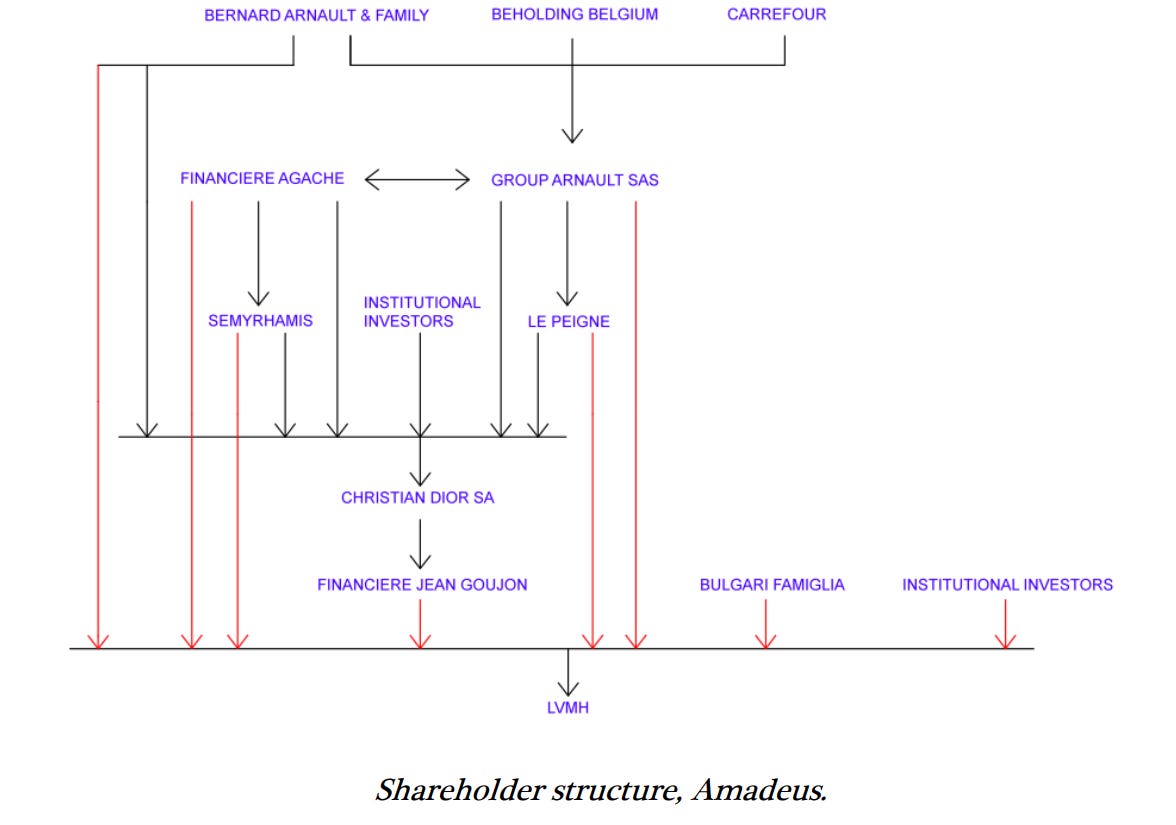

LVMH Shareholder Structure

Let’s move up the ladder. LVMH’s ownership is far more complicated. I have yet to find a clear chart with ownership percentages, so the below will do for now.

When this structure was published in 2013 (yes I know… it’s quite dated), Arnault controlled 65% of the voting rights through his various entities.

The family HoldCo (Bernard Arnault & Family, top left above) directly owns less than 1% of LVMH but takes control through other companies as financial and holding companies.

Per our prior discussion on cascading, remember how we brought in outside investors at various levels? Notice above that institutional investors sit at two levels: 1) directly above Christian Dior SA and 2) directly above LVMH. The purpose of outside money is to 1) reduce the upfront cash required at time of acquisition or 2) sell a minority stake later in the ownership period to generate cash proceeds.

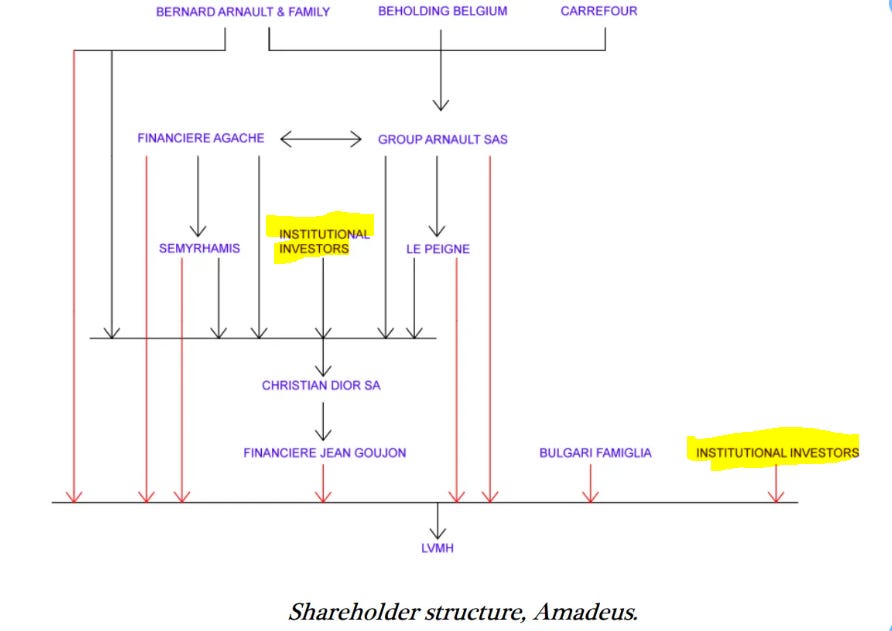

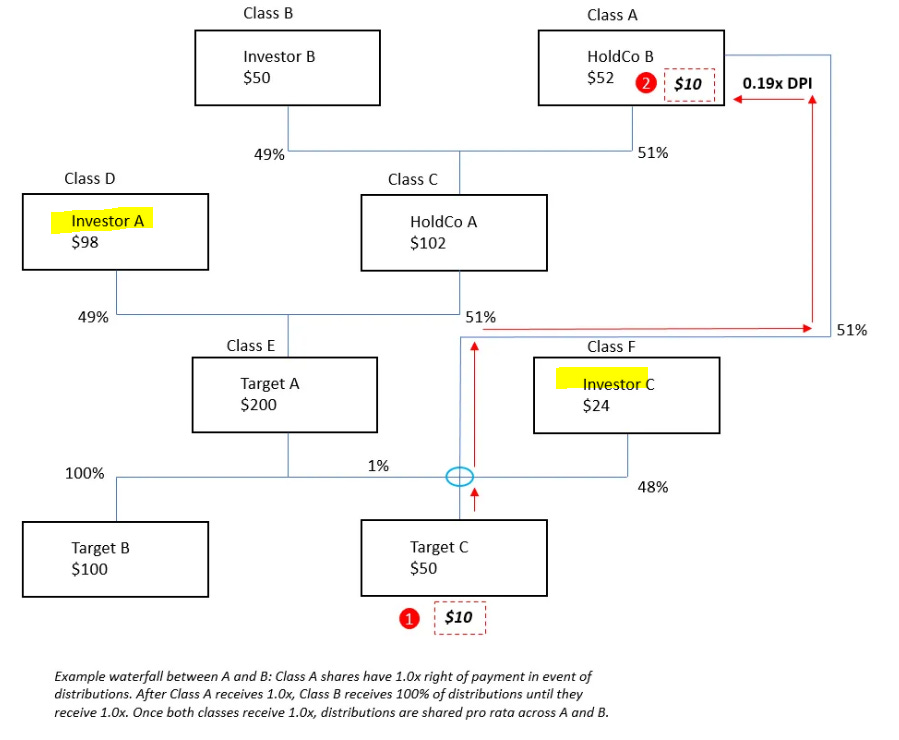

This is very similar to Investor A and C in the prior post snipped below.

Effectively, using the snip above while ignoring the ownership percentages, here is the similarity comparing both structures.

Target A = Christian Dior

Investor A = Christian Dior institutional investor

Investor C = LVMH institutional investor

Target C = LVMH

HoldCo B = Bernard Arnault & Family

Yes, Christian Dior has an extra layer through Financiere Jean Goujon that Target A does not show, but the general comparison is true across both structures.

So, we can see that we were fairly close in capturing how the cascading structure appears in practice… using none other than LVMH as the example!

More Details From the Universal Registration Document

A general rule of thumb when reading reporting documents is to start at the back and work towards the front. Most of the important information is hidden in the back, as is the case here.

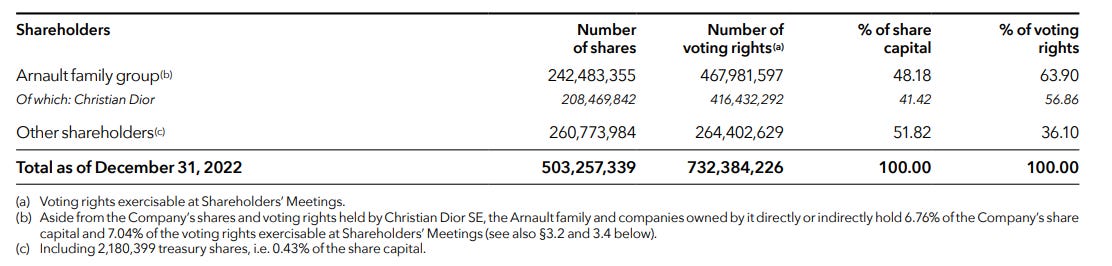

So, I jumped to the very end and found useful information on the ownership structure (of course, on page 345 out of 364 pages!)

The Free Float that sits to the right of LVMH represents the Other Investors in the below table.

Here is what the document says directly:

As of December 31, 2022, the Arnault family group – comprising the Arnault family and the companies it controls, including Agache SCA – owned, directly and indirectly, 48.18% of the share capital of the Company (i.e. 242,483,355 shares) and 63.90% of the voting rights that may be exercised at Shareholders’ Meetings, which breaks down as follows:

• 41.42% of the Company’s share capital (208,469,842 shares) and 56.86% of the voting rights exercisable at Shareholders’ Meetings, via Christian Dior SE; and

• 6.76% of the share capital of the Company (i.e. 34,013,513 shares) and 7.04% of the voting rights that may be exercised at Shareholders’ Meetings via the Arnault family and other Arnault family group companies.

*I added in the bold*

Two things:

Control is split directly and indirectly. Directly, the Arnault family holds 6.76% of share capital and 7.04% voting rights. Indirectly, through Christian Dior which is majority controlled by the Family, the Arnault’s own 41.42% of the share capital and 56.86% of the voting rights.

Total Arnault control of LVMH stands at 63.90%

They get an additional 15.74% points of control through double voting shares (48.16% —> 63.90%)

Certain shares have more advantageous voting rights than others, of which the Arnault family holds most of these more favorable voting shares.

Total shares of 503,257,239.

The Arnault family holds 242,483,355 shares, or 48.18% of the total amount.

Even better, the Arnault family holds most of the voting shares.

When factoring in voting shares, the Arnault family percentage of voting rights raises to 63.90% while Other Shareholders falls to 36.10% from 51.82% percentage of share capital.

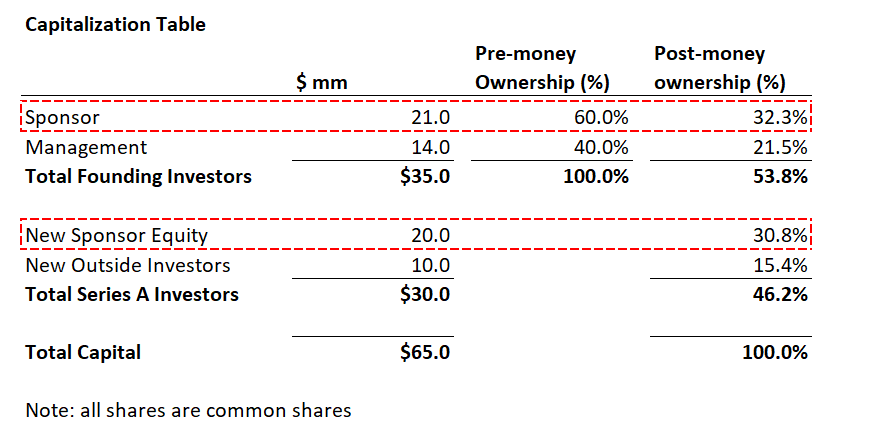

The voting’s rights that Arnault Family holds dilutes the control of the % of share capital held by other shareholders. This is very similar to yesterday’s example where the outside investors contribute 1/3 of the new money but receive 15% post-money ownership. In the below cap table example, dilution comes from the sponsor promote. In LVMH’s case, control dilution is in the form of double voting shares mostly held by the Arnault’s.

This is an important concept of structuring advantageous voting rights to the Family shares, which has not been discussed in the prior two cascading articles.

So, another example to 1) maintain majority control and 2) reduce the equity commitment is to hold advantageous voting shares over other investors, giving you additional voting control.

Hopefully this is a helpful example of an additional mechanism to maintain control ([double] voting shares).

++

Until next time.

John Galt