6. Cascading Ownership (Part 2/3)

6. Cascading Ownership (Part 2/3)

Venture Capital Financing, Preferred Equity, Repayment Rights and Structured Equity

Let’s continue to explore the cascading ownership idea. In the last post, we looked at how cascading can 1) maintain control while 2) reducing upfront required capital.

We will further explore this structure, briefly addressing the nuances and looking at how the sponsor can achieve this goal through other means of structuring.

Let’s begin with an example.

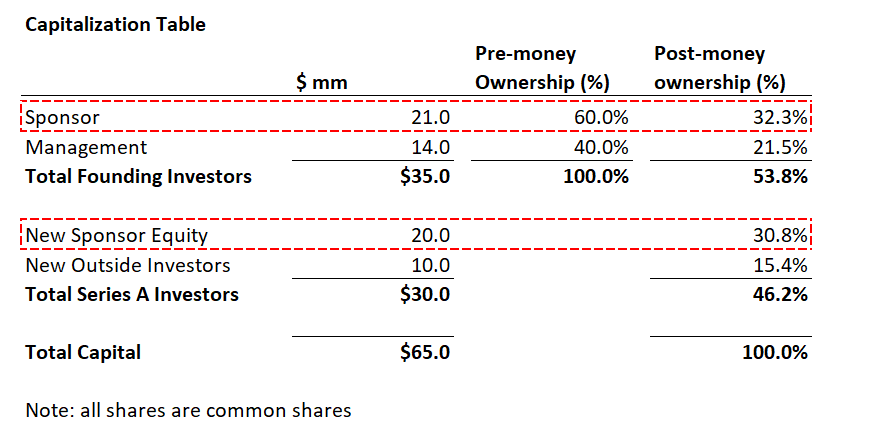

There are 3 parties below: 1) the sponsor 2) management and 3) new outside investors. The sponsor wants to raise outside capital for a development deal while 1) minimizing the required equity commitment and 2) preserving maximum control.

The deal itself isn’t important, but this is pulled from a transaction where the sponsor raised capital to finance new unit development in a new market.

The example below illustrates one way that the sponsor can achieve this goal…mirroring venture capital financing structures.

Double-clicking on the note, these are all common shares. We have yet to dive into structuring via preferred vs common.

Notice that the sponsor maintains combined ownership of 63.1%. Even more importantly, they achieve this by only committing $20mm of the $65mm total capital.

If this were all 1:1, the $20mm of hard dollars would give them 30.8% ownership, well below majority control (excludes the 32.3% ownership points of promote).

Here’s the spin: the Total Founding Investors capital of $35mm is NOT hard dollars put into the business. Think of this as promote. The sponsor and management did not actually contribute $21mm and $14mm of capital, respectively.

Rather, they allocated ownership points to themselves and the dollar amounts back into the desired ownership, illustratively.

This is very important because the sponsor and management effectively hold 54% control simply through structuring… no hard dollars were actually committed to this pool / tranche of the cap stack.

In other words, the sponsor simply awarded themselves 32% ownership for sweat equity and for managing the deal. This very similarly resembles venture capital financing in which founders retain a significant equity percentage without having to contribute the equity 1:1 to receive those shares.

The promote gives the sponsor (equity) leverage without having to raise debt from lenders.

Look down to the Series A tranche now. The $20mm of sponsor equity does in fact represent new hard dollars contributed. That gives the sponsor 31% ownership.

Remember, the sponsor would like to reduce its required equity while maintaining control, so they bring in $10mm (15%) outside capital to fund the remaining equity need.

So, new outside capital contributed 1/3 or 33% of the new money ($30mm) but only received 15% post-money ownership. This dilution is simply a result of the sponsor promote.

That’s the beauty of other people’s money (OPM) and structuring sponsor promote!

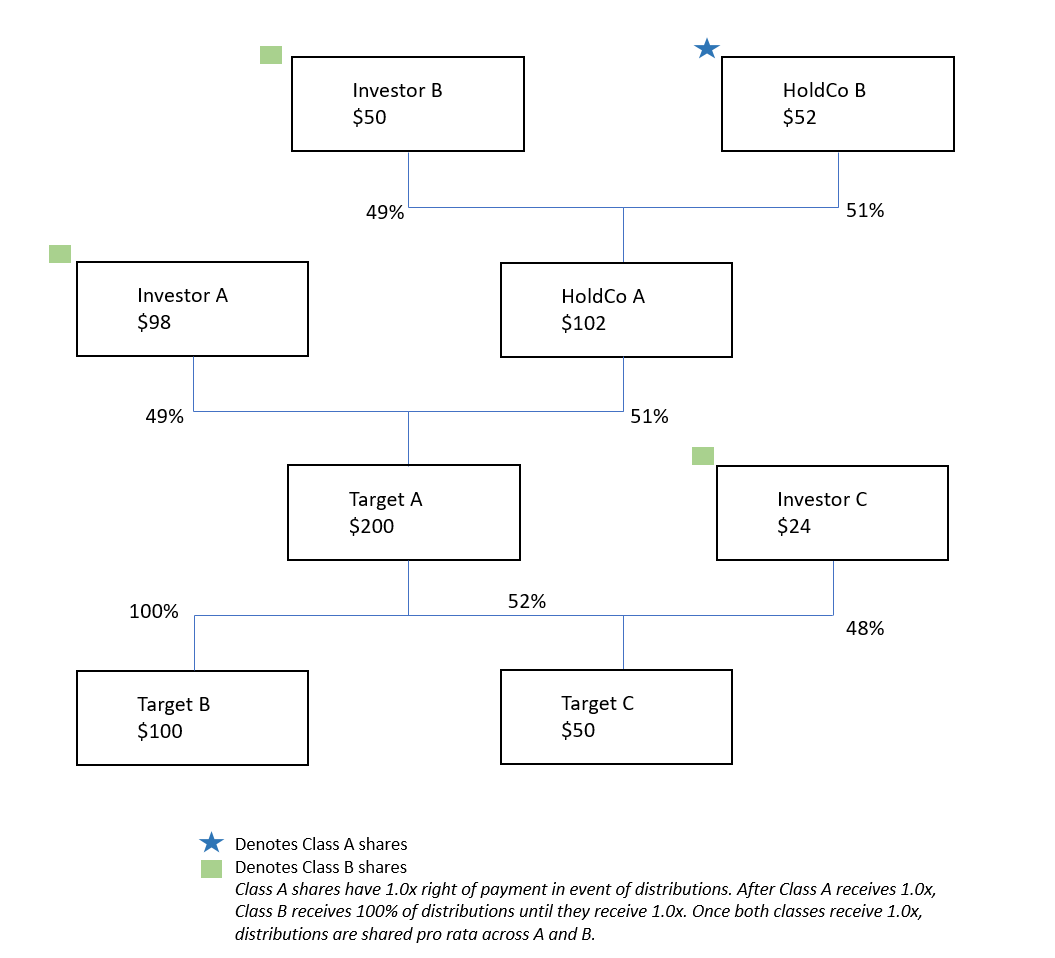

Structuring Equity

Another idea is to structure the equity such that the sponsor benefits from seniority and terms.

The dividend recap section of article 4 highlights this dynamic in an example. Please reference this article for a more fulsome example.

Effectively, you can structure the sponsor equity such that it receives first right of payment in the event of distributions (and liquidation).

Let’s say that the $52mm of HoldCo B equity is Class A while Investor B holds Class B shares. Class A shares receive 100% of distributions until repaid to 1.0x before the Class B shares receive a single dollar.

After Class A is paid back to 1.0x, Class B gets paid to 1.0x.

The third part of the waterfall distributes excess money pro rata to Class A and Class B.

This is just one example. You can be more aggressive or conservative in structuring the repayment rights between classes.

For example, Class A gets 1.0x, you skip step 2 and immediately distribute any excess pro rata between A and B. That could result in a scenario where A stands at 1.3x while B is at 0.3x distributions to paid-in capital (DPI).

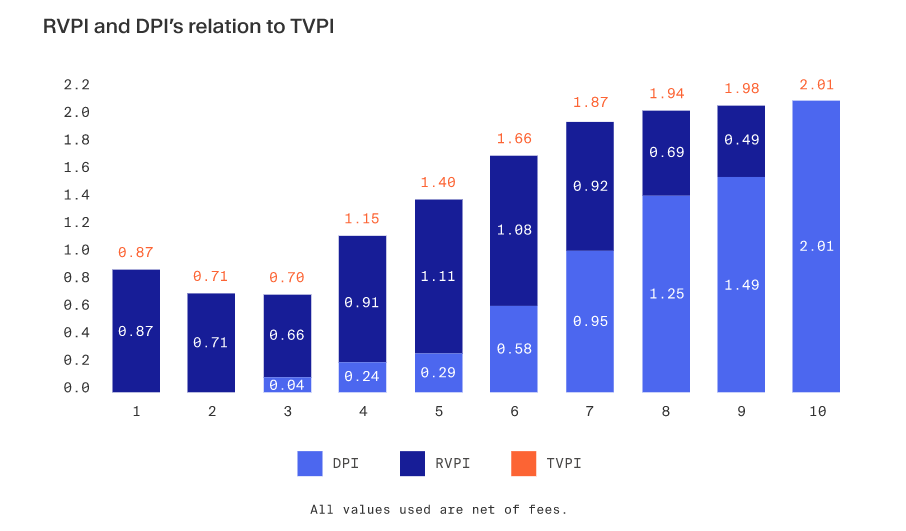

Quickly on DPI

DPI measures cumulative value of distributions paid to the investors relative to the money invested. It is expressed as a multiple of investors’ paid-in investment capital. Investors often see Total Value to Paid-in Capital (TVPI). This is the sum of DPI + Residual Value to Paid-in Capital (RVPI).

In other words, TVPI is DPI (money received or distributed) + RVPI (unrealized mark / yet to distribute).

It is very difficult for managers to translate TVPI to DPI, especially in the venture capital world where RVPI is grossly overstated.

Oftentimes, in VC, you’ll be stuck at point 5, 6, or 7 and never reach point 10.

So, with repayment rights, Class A can capture a disproportionate share of DPI in the early years before Class B sees any DPI.

Back to our cascading example…

Structuring different classes of equity (with different rights of payment in the event of distributions) can reduce distribution leakage to HoldCo B.

With structured equity, rather than distributions flowing up the structure pro rata, it will follow the waterfalls for A and B shares at each level.

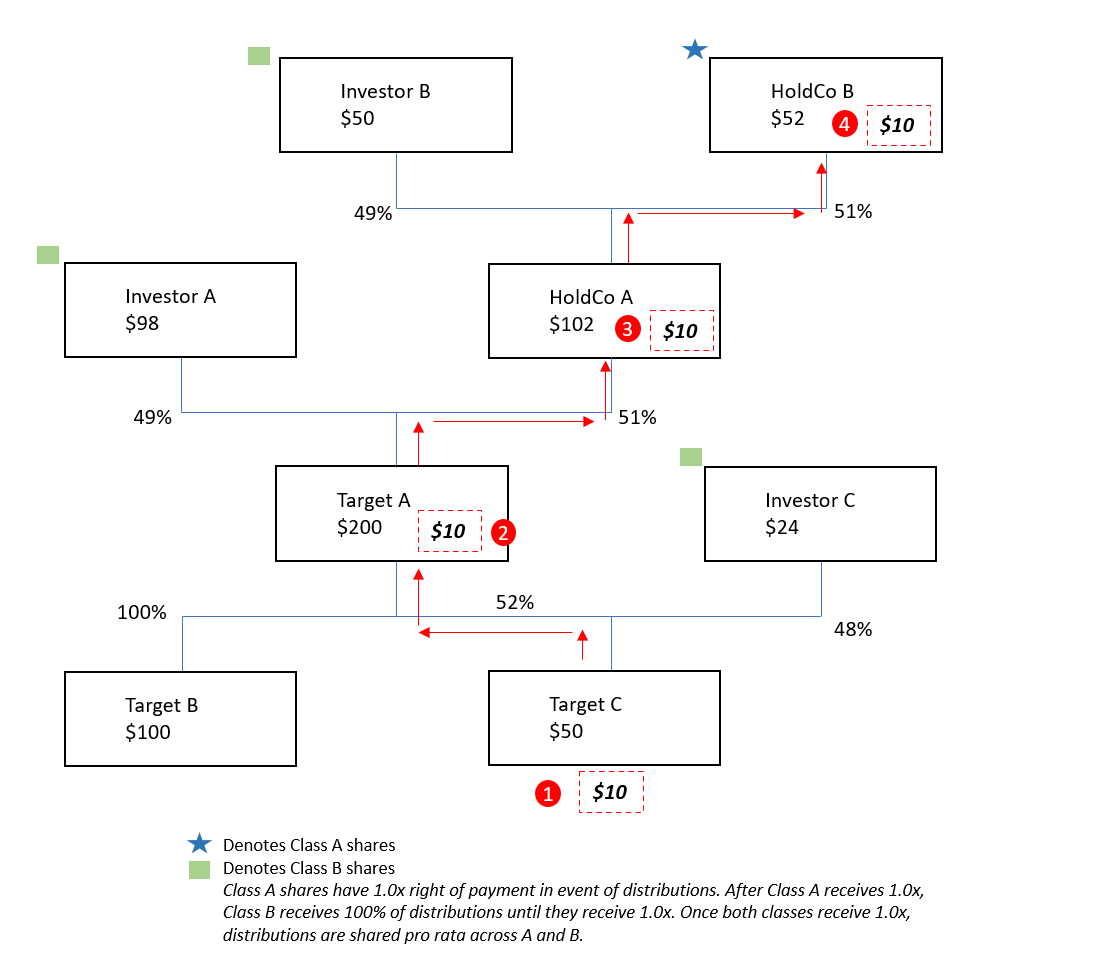

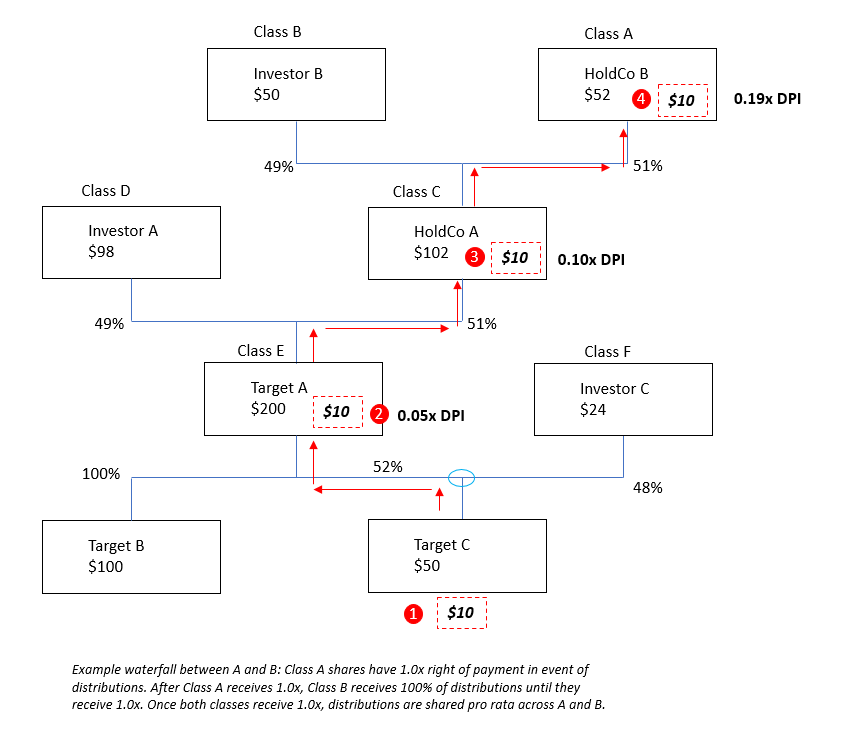

Here’s an example of $10 of distributions coming from Target C.

The reason that the $10 flows all the way to HoldCo B, without leakage, is because of the 1.0x repayment right.

Meaning, HoldCo B will still receive 100% of the next $42 of distributions, which will bring them to 1.0x.

This brings up the more complicated question at each intersection. As the $10 flows up, the first intersection is between Target A and Investor C (circled in blue below).

Do HoldCo B’s Class A shares have any influence at this first intersection? I don’t think so.

Then, we have to refine the cascading structure such that there are additional share classes each with the same rights of payment.

Note the waterfall description below the charts. Assume this waterfall holds true for each share class that has a shared interest in a subsidiary.

The “>” indicates who gets paid first when distributions flow through.

Class A > Class B

Class C > Class D

Class E > Class F

In effect, Class A > Class F!

That’s how you control the first intersection of the distribution from Target C (circled in blue above) from the standpoint of HoldCo B.

So, you can in fact send the distribution all the way up to Class A from Target C if you have the appropriate terms structured in to each class of equity.

Note that this has not been vetted by lawyers and is surely subject to additional nuance! The purpose of this article is to underscore the ability to reduce equity and maintain control through structuring / cascading.

That LVMH and other family holding companies are structured in this fashion is a testament to the fact that it’s possible.

One other side note. Look at Target C. They have separate outside investors. Part of LVMH’s strategy to raise capital has been to publicly list subsidiaries. Arnault will take a sub public to raise minority equity capital for other uses.

Back to our example. What incentive exists for Investor B? Well, one incentive is to directly invest alongside the sponsor (HoldCo B). In a PE context, this co-invest can bypass fees associated with a blind commitment to the sponsor’s fund.

Secondly, if the sponsor has a top-tier track record, many investors will want to invest directly alongside them. This certainly feels true of any LVMH deal if presented to a pool of potential investors (or Veritas!).

Additionally, you can transfer operating assets to each HoldCo to further entice new investors at each level… in effect changing, say, HoldCo A to an entity that actually houses OpCo assets.

A quick reminder that this discussion has fully excluded any debt restriction considerations. For instance, we have not addressed restricted payment (RP) capacity governed by credit agreements (CA). For example, Target C may have an existing credit agreement that limits RP capacity / leakage outside of the credit group.

This makes sense intuitively. If I’m a lender to Target C, I will want to limit how much value leaks from the credit group (what’s protected and governed by the CA…my collateral). So, there will be stipulations that limit distribution capacity and asset transfers to unrestricted subsidiaries. We can dive into this further another day.

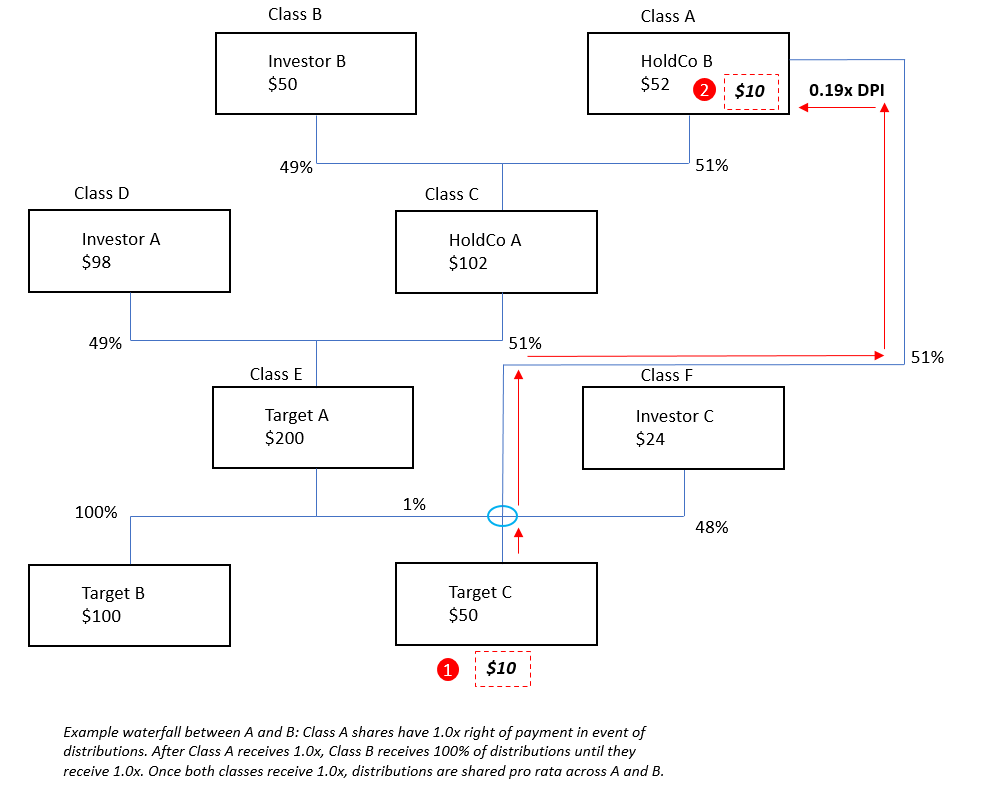

Lastly, let’s assume the various share classes are too complicated or not feasible. Here’s an example where you bring the Target C asset closer to HoldCo B, thereby reducing leakage from Investor A and B.

The old structure showed Target A owning 52% of Target C and Investor C owning the remaining 48%.

Now, we’re bringing HoldCo B directly into Target C’s cap stack via a 51% ownership (you do this at time of acquiring Target C). Structure this exactly like the first example in the article! Remember, in the first example, the sponsor held 54% without actually putting any hard dollars into the capital structure.

So, with this new structure, you can still structure the equity such that HoldCo B has rights of repayment over Investor C. The asset is closer to HoldCo B so there’s less leakage and fewer intersections that the distribution must cross.

Instead, the distribution hits the first intersection and is fully sent to HoldCo B until 1.0x repayment of Class A.

Re-snipping the first image as a rough illustration as to what Target C’s cap table may look like in this scenario.

Maybe we’ll look at more pref / common structures and credit agreements in the next post.

++

Until next time.

John Galt