27. Continuation Vehicles (Cont'd)

Further detail on continuation vehicle dynamics - continued from post 3

Let’s pick back up the discussion on continuation vehicles in the context of private equity exits. We originally introduced this topic in post 3, which can serve as a good refresher before we dive into the math below.

As a quick refresher, continuation vehicles are a somewhat recent ‘innovation’ in private equity whereby the owner of an asset (the private equity firm “PE firm” or “the sponsor”) can equity recapitalize the business by carving it out of the fund and into a new vehicle.

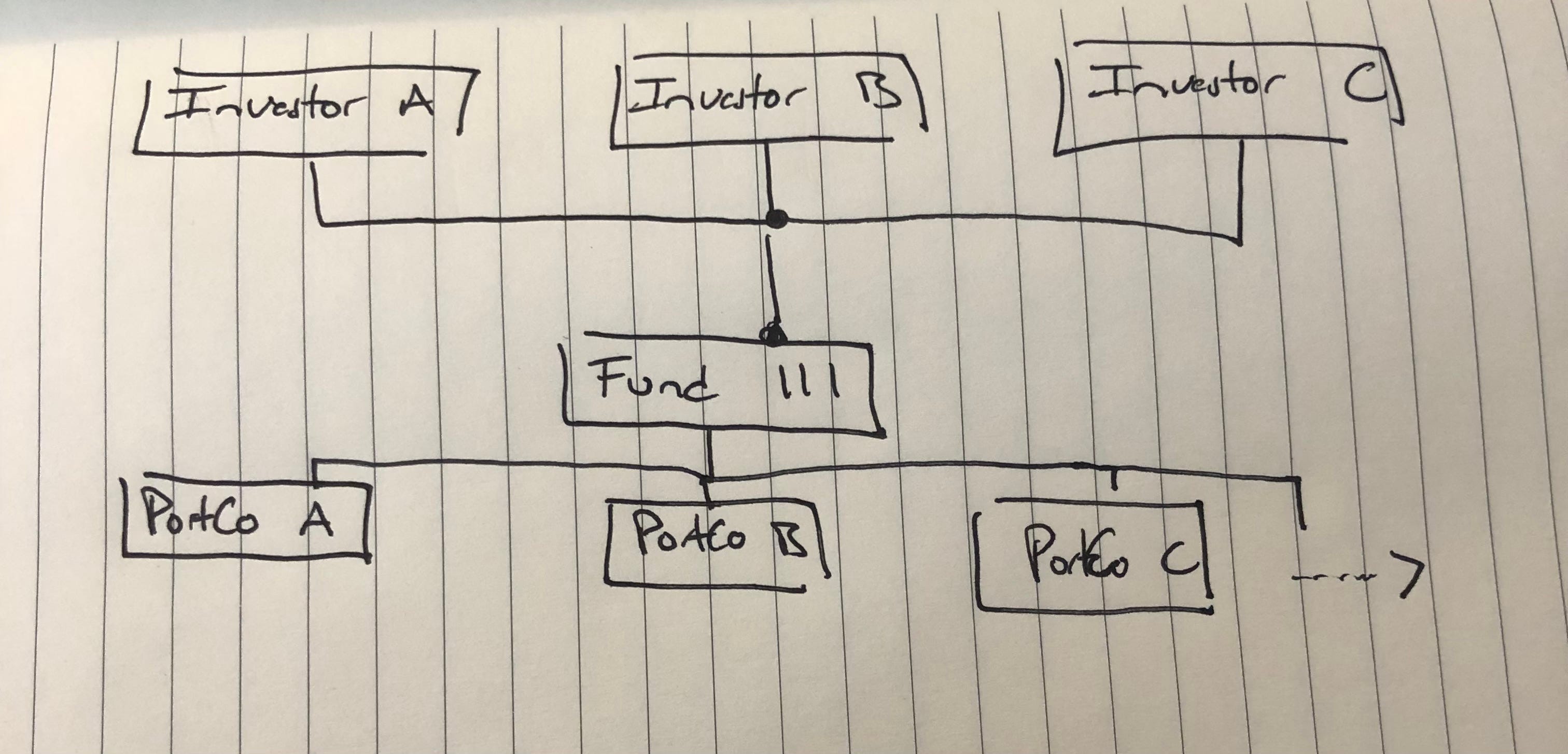

Below is a simple illustration of the anatomy of a private equity fund. Fund III, in this case, is capitalized with investment money from Investors A, B and C, known as limited partners [of the fund] (“LPs”). The fund is managed by the sponsor, known as the general partner (“GP”).

The GP will manage the fund and make investments into portfolio companies (“portco”) to deploy the capital. These funds typically have 10-year structures with two 1-year extension options.

In other words, if a sponsor raises a fund in 2024, the LPs are committing capital to the fund for a 10-year period through 2034. However, near the end of the fund, the sponsor can extend the fund life for 1-year with a sufficient amount of LP approval votes. This typically happens if assets remain in the fund as it approaches expiration / the sponsor needs more time to liquidate and exit the last few investments.

Now let’s look at the picture:

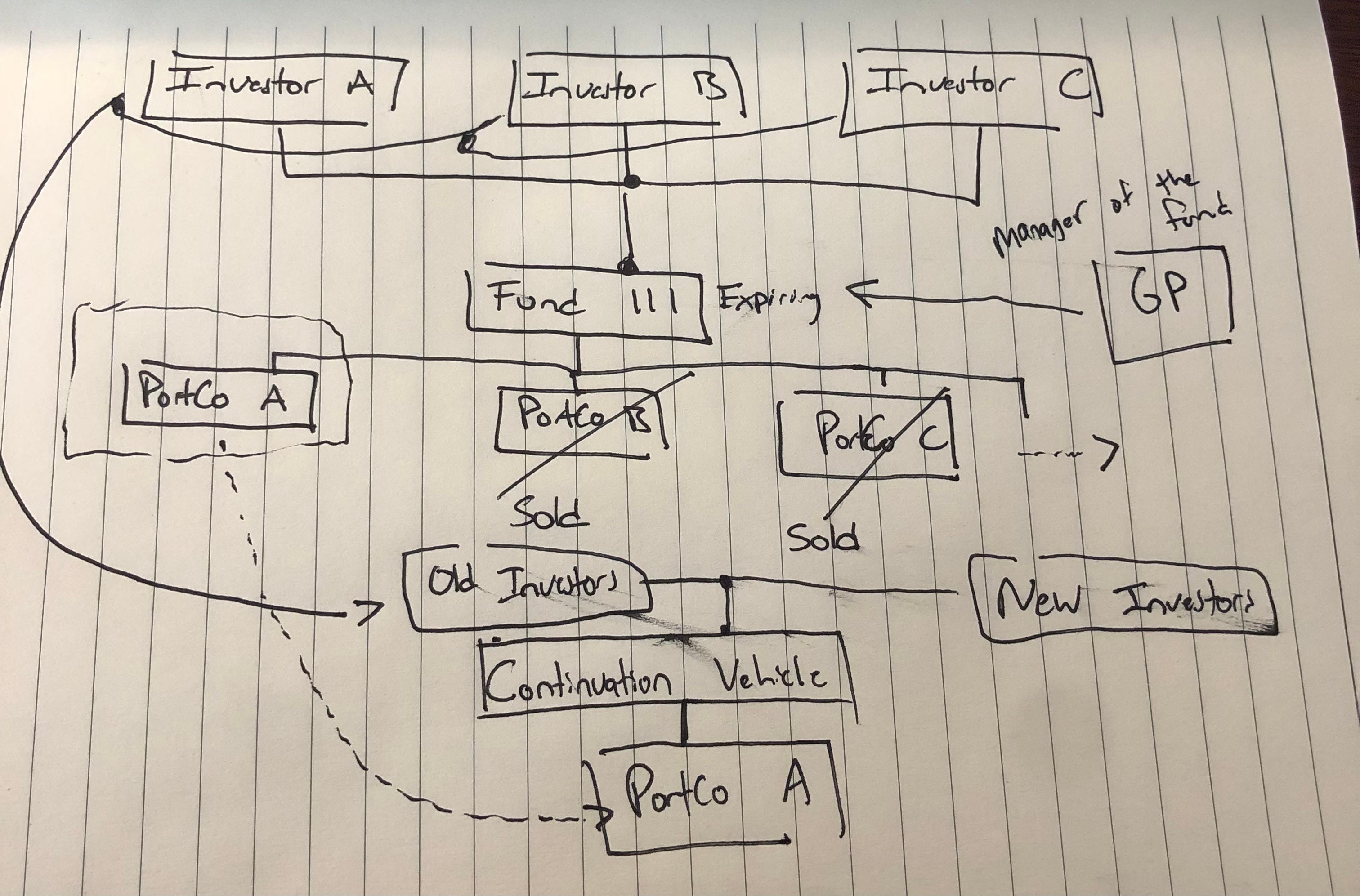

Continuation funds can arise for many reasons. In our discussion today, let’s assume Fund III is expiring. The fund has already liquidated its investments in the other portfolio companies - all that remains is portfolio company A.

But what if the sponsor doesn’t want to be forced to sell this investment simply because its fund life is expiring? For instance, the investment might be marked at 2.0x and the sponsor believes it will ultimately be worth 4.0x. They would not want to sell it now due to the fund expiring.

So what can they do? One option is a continuation vehicle. Effectively, the sponsor carves out the asset from the fund structure into a new entity, the continuation vehicle (“CV”).

The picture gets a bit messy… and yes, I smeared the ink to unfortunately make it messier…

Let’s walk through this. To recap, the cause for all of this shuffling is that Fund III is expiring - it’s like a business closing… the sponsor needs to clear out the assets from the fund and return capital back to the fund’s investors.

Portco B and portco C have been sold. Portco A remains. The sponsor thinks there is further upside and does not want to fully exit the investment at this stage.

So, portco A is carved out and moved into the CV, which is capitalized by old investors (A, B and C) who choose to roll into this transaction and new investors who backstop those existing investors who choose not to roll.

Put differently, investors in Fund III receive an option to participate in the continuation vehicle by rolling their pro rata stake into the new entity. Those who choose not to roll will receive a cash distribution in-line with where the investment is currently marked. They will be backstopped / replaced by new money from the CV’s new investors.

This is how a continuation vehicle works at a very high level.

Now, let’s take a look at the carry math to understand why GP’s love these trades.

Continuation Vehicle Carry Waterfall

Carry is short for carried interest, which represents a portion of the investment gains that go to the GP / sponsor of the fund.

Marks, which we have referenced, refers to the return of the investment relative to the cost. Marks refer to multiple of invested capital (MOIC). So, in any deal, the cost basis is 1.0x for a new investment. You invest $1 on day 1 and it’s immediately marked at 1.0x. $1 is the cost basis.

Now, let’s say the business has performed well and you have earned a 100% return. Think about this like a stock. In the private equity world, this would then be marked at 2.0x. Your $1 has turned into $2.

If you sell at $2, how do the gains get split between the LPs and GP?

Very simply, the LP first gets their cost basis returned - they receive their original $1.

Then, the gains are split 80 / 20 between the LPs and GP. So, of the incremental gains of $1, the LP gets 80 cents and the GP gets 20 cents.

The 20 cents to the GP is what we call carry. Carry is what has made billionaires in private equity.

With the basics behind us, let’s now look at the waterfall for a CV deal. Fair warning this may get a bit detailed. If you’re not interested in the details, you can end the post here.

Otherwise, let’s move on.

To keep it simple, let’s assume portfolio company A is a ‘performing asset’ - meaning, the investment has done well and is marked above cost. We can also look at ‘underperforming assets’ in the context of a CV, but maybe that’s for another day.

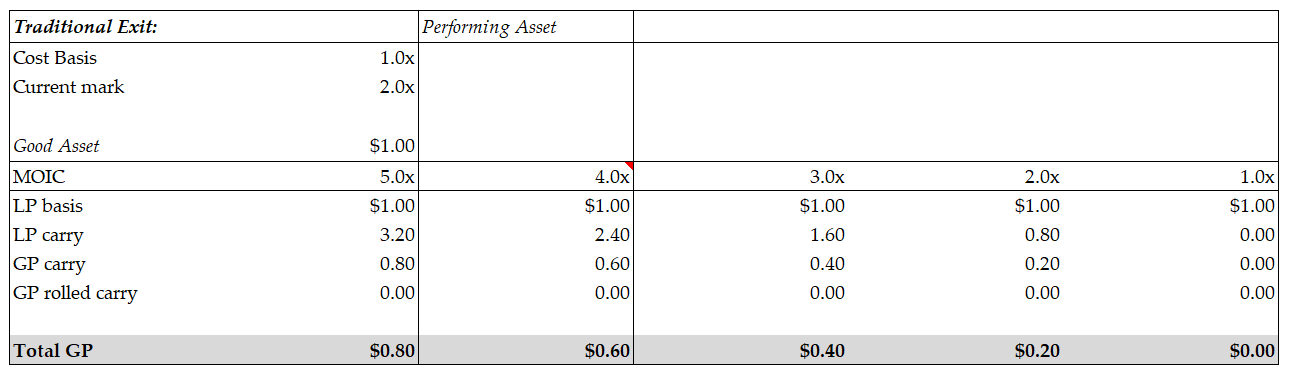

So the setup below - we have a performing asset with a cost basis of 1.0x that is currently marked at 2.0x. We, the sponsor, want to do a continuation fund at 2.0x because our fund is expiring but we think there remains further upside to 4.0x.

Here is what the carry waterfall looks like if we were to simply sell the business in a traditional exit. Notice 4.0x is the base case, but if you look to the right you’ll see the 2.0x column, with carry splits to the LP and GP that we discussed above.

So, if we were to simply sell this investment at 4.0x, the LP would receive their $1 of cost basis. Then, the remaining $3 would be split 80 / 20 between the LP and GP. The LP receives $2.40 of gains and the GP receives $0.60 of carry.

Great, this is a homerun for the GP. They exited at 4.0x and earned $0.60 of carry. But can they do better through engineering?

Now, as mentioned, let’s instead assume that the sponsor does a continuation vehicle when the investment is marked at 2.0x. In our crude illustration above, this means that we are assuming portco A is carved out of the fund when it’s marked at 2.0x. That’s the value at which the continuation vehicle trade clears.

The second part of this table shows the waterfall if a CV happened at 2.0x and you later exit at the same 4.0x that we assumed in a traditional exit (if we sold the business outright).

What’s important here is the ‘Incremental to GP’. The math shows that the GP can earn incremental carry if they do a continuation vehicle compared to a traditional exit.

Further, the more upside there is between the current mark and future exit value the more a CV exit makes sense. Notice how the incremental carry decreases as you move right and assume the final exit is closer to the mark at which you did the CV deal (2.0x).

Let’s go through each row in detail so we can see how the math works.

LP Basis - this assumes the LPs roll at 2.0x, so $2, less the GP carry at 2.0x. This is crucial - a CV triggers carry to be allocated to the GP at time of the CV… even though the asset hasn’t gone through a traditional exit. In other words, when the asset is carved out of the fund, the GP earns the $0.20 of carry.

In most cases, rolled LPs will require that the GP roll this carry into the continuation fund rather than crystalize the carry and take it off the table. Think of this as a CV triggering carry allocation to the GP at whatever mark the CV occurs at. In this case, the GP earns $0.20 at time of CV and rolls this carry into the deal, dubbed ‘GP rolled carry’.

The LP basis is then the $2 less the $0.20 of GP carry. This is effectively a step up in the LPs cost basis! And, the cost basis is not $2 because $0.20 of that has already been allocated to the GP as carry. I hope this makes sense. The key is that the LPs cost basis has stepped up from $1 to $1.80.

LP carry - this is 80% of the incremental gain above LP basis and GP rolled carry. The new twist here compared to the simple example is that we deduct GP rolled carry. Why? because the LP no longer has carry rights to this slice of equity… it’s already been allocated to the GP.

The math is $4 - $1.80 = $2.2 —> MOIC less LP basis

Then, $2.2 - $0.40 = $1.80 (subject to carry) —> less GP rolled carry. The GP rolled carry is $0.40 because it was rolled into the CV at $0.20 (at a 2.0x valuation) and the valuation at exit has doubled (4.0x) so the rolled carry is now worth $0.40.

Then, $1.80 * 80% = $1.44 —> gains to the LP.

$1.80 * 20% = $0.36 —> GP carry.

GP carry - the calc is above, but this is 20% of the incremental gains that are subject to carry. The subject to carry amount is $1.80. 80% goes to the LP and 20% goes to the GP.

GP rolled carry - we also calculated this above. But simply, it’s the stepped up valuation of the $0.20 of GP carry that was rolled into the continuation vehicle.

So, total carry to the GP is $0.36 + $0.40 = $0.76.

That’s more than the $0.60 the GP earns in a traditional sale! The takeaway is that CVs allow GPs to earn incremental carry compared to a traditional exit.

Conclusion

As an LP, it’s crucial that you understand the carry dynamics to the GP when you are invited to participate in a continuation vehicle. The starting point is the reason for the CV. Then, you can dig into details around how much carry is allocated to the GP at time of the CV, whether they are rolling all of the carry into the new deal, the new LP basis, the expected incremental carry to the GP, etc.

Essentially, the LP will want to understand how much value is being transferred from rolled LPs to the GP - as continuation funds reset the carry basis for GPs… which is how GPs can earn incremental carry.

This math is a starting point to understand why GPs love these deals, and why we have seen an explosion in continuation funds in recent years.

Thank you for reading.

++

Until next time.

John Galt