13. Leveraged Finance Springing Maturity (Surgery Partners Example)

A review of Surgery Partners' springing maturities

Let’s look at another common leveraged finance concept: springing maturity. In the below example, we’ll see how a company can have several tranches of debt each with a springing maturity.

At a high level, when looking at a company’s capital structure, the most senior debt usually must mature before junior debt. So, a revolver matures before a term loan, a term loan matures before secured notes, secured notes mature before unsecured notes, etc.

The reason for this is that if you have a senior tranche maturing after a junior tranche, then the senior tranche is effectively structurally subordinate to the junior tranche. For example, your revolver matures on June 1, 2025 while your term loan matures on June 1, 2024. The revolver is the more senior tranche of debt which takes priority in the event of liquidation. It’s the safest piece of debt in a cap structure. But, since the term loan matures before the revolver, it becomes structurally senior to the revolver. This is because the term loan is paid back before the revolver gets paid, assuming no refinancing of the term loan.

That’s the basic logic of forming a capital structure - more senior debt demands earlier maturities than the junior debt beneath it. But, what we’ll see is that you can in fact have a revolver with a maturity after the term loan’s maturity. The mechanism that enables this is a springing maturity, which, as we will see, bumps the revolver ahead of the term loan if the term loan is not refinanced.

Let’s look at an example.

Surgery Partners

Bain initially bought a stake in Surgery Partners (NASDAQ: SGRY) from HIG in 2017. HIG originally invested in the business in 2010 and took the company public in 2015.

We’re only interested in the capital structure at this point… so let’s take a look.

On Jan. 27th, 2021, Surgery Partners entered into a 5th amendment to its credit agreement achieving a few things including 1) incurring $50mm of incremental revolver commitments and 2) extend the maturity date of the revolver to Feb 1, 2026. You can read the amendment here.

Per the amendment, the revolver is subject to a springing maturity date of Aug. 31, 2024, if on that date there are outstanding term loans that have not been replaced or refinanced with a maturity date not earlier than Feb. 1, 2026.

At the time of the 5th amendment, the $1.4bn first lien term loan was set to mature on Aug. 31, 2024.

Then, on May 3, 2021, the Company entered into its 6th amendment, found here, pursuant to which it refinanced the existing term loan for a new $1.55bn facility maturing on Aug. 31, 2026. The new term loan is subject to a springing maturity date of Aug. 1, 2025, if on that date at least $185mm of the 6.75% unsecured notes due 2025 are outstanding and have not been refinanced with debt that matures on or prior to 91 days after Aug. 31, 2026. You can read the language on page 66 of the amendment.

Let’s pause to recap - 1) the maturity of the revolver depends on the maturity date of the new term loan and 2) the maturity date of the new term loan depends on whether at least $185mm of the unsecured notes due 2025 is still outstanding on Apr. 1, 2025.

Remember, the purpose of these springing maturities is such that the senior debt matures either together with or prior to junior debt. In Surgery Partners’ case, we’re seeing how several springing maturity mechanisms accomplish this goal and appease each lender.

Determining the Maturity Date

In each amendment, you can find a section (2(d) in the 5th amendment) that explains the maturity date. Here is what the 5th amendment looks like with respect to the revolver (pg. 3).

The “on or prior to” language is important. It effectively means the springing maturity test is an ongoing test that is in effect unless and until satisfied by Aug. 31, 2024. If the language simply stated “on” then the test could only be conducted on Aug. 31, 2024, not beforehand.

The term loan has a similar springer as seen a few pictures above. However, while the revolver’s action is whether the term loan matures before the revolver, the term loan’s action is whether less than $185mm of 2025 notes mature prior to the term loan.

Let’s go back to this picture.

The new term loan matures on Aug. 31, 2026 but will spring to April 1, 2025 if at least $185mm of 2025 unsecured notes has not been repaid or refinanced.

The revolver matures on Feb. 1, 2026 but will spring to Aug. 31, 2024 if the term loan has not been fully repaid or refinanced with debt maturing after the revolver.

Here’s the issue for Surgery Partners -

Let’s think about the term loan as maturing on Aug. 31, 2026. This could be accelerated until April 1, 2025. But, the revolver’s maturity will not be accelerated since on Aug. 31, 2024 (the last date at which the revolver could accelerate/spring), the term loans mature on Aug. 31, 2026.

So, the term loan could still mature ahead of the revolver given that the springing maturity could still occur on April 1, 2025 (but the revolver is past its springer date!!). From the revolving lenders standpoint, this is a terrible scenario.

How to think about the right maturity date

Another way to think about the maturity date is to treat the tranche as if it will spring. For the term loan, treat the maturity as April 1, 2025 until it takes action to avoid the springing maturity. So, the TL’s maturity is the springer date of April 1, 2025, until it takes action to become Aug. 31, 2026.

Also, if Surgery Partners has not repaid or refinanced a sufficient amount of the 2025 unsecured notes by Aug. 31, 2024 (this is the revolver’s springing maturity date), then on Aug. 31, 2024, the term loan’s maturity would be earlier than the revolver’s maturity (the term loan springs) and, as a result, the revolver would immediately come due.

Meaning, Surgery Partners would need to ensure that less than $185mm of unsecured notes due 2025 have not been repaid or refi’d by Aug. 31. 2024, not April 1, 2025.

This picture for a 3rd time! The important date here is Aug. 31, 2024.

Conclusion

Springing maturities are common terms found in credit docs. It ensures appropriate structural seniority between the tranches of debt in a situation where more junior debt has a maturity inside of senior debt maturities.

Surgery Partners is also a great example of a company that may have several springing maturities across docs. It’s important to note the actions that trigger an acceleration and understand structural seniority/subordination in various scenarios.

All of this is particularly important from the lenders perspective. But, if you’re the bank advising the company, it’s also important to understand these dynamics to craft an appropriate capital structure.

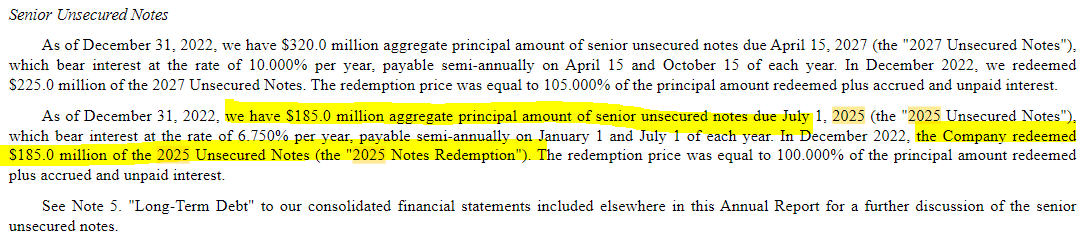

P.S. - If you look at the 10-K posted on March 1, 2023, you’ll notice that the Company redeemed $185mm of the unsecured notes due 2025 (redeemed 50% to go from $370mm to $185mm outstanding).

It seems like the source of funds for the notes repayment was an equity raise, although I spent little time confirming this outside what’s listed in the cash flow statement.

So, from this walk-through, we can now infer the logic around getting the 6.750% unsecured notes from $370mm to $185mm!

Hope you found this helpful.

++

Until next time.

John Galt