12. The Retail Revival

12. The Retail Revival

A brief history of retail and Sam Zell

I found Doug Stephens’ The Retail Revival for $1 in a bookstore and decided to give it a read. It looked interesting, and I’ve been wanting to read more about retail.

A common theme throughout the book: retail has fundamentally changed since the late 90s and companies must adapt or suffer a slow death.

Industries filled with brilliant executives have crumbled because of a failure to properly acknowledge the magnitude of the impact that specific changes would have on companies.

And this:

Some of the world’s most respected minds have similarly underestimated the volume and velocity of change in their markets.

Over the last ~50 years, retail has benefited from a number of factors which are less relevant in today’s world. Retail has fundamentally changed, according to Stephens.

The Birth of 1960s Retail

There is one recipe that all retailers dream of - lots of new customers all of whom want the same thing. In other words, large new volume of business within the same narrow selection of SKUs.

This was the case in the 1960s and why dozens of familiar brands were founded during this time (especially 1962, being the birth year for Walmart, Target, Kmart and Kohl’s).

The list also includes:

Best Buy (1966)

Gap (1969)

Limited Brands (1963)

Calvin Klein (1968)

Crate and Barrel (1962)

Peet’s Coffee & Tea (1966)

PepsiCo (1965)

Petco (1965)

Pier 1 (1962)

Rite Aid (1962)

The North Face (1966)

Vans (1966)

Among many others…

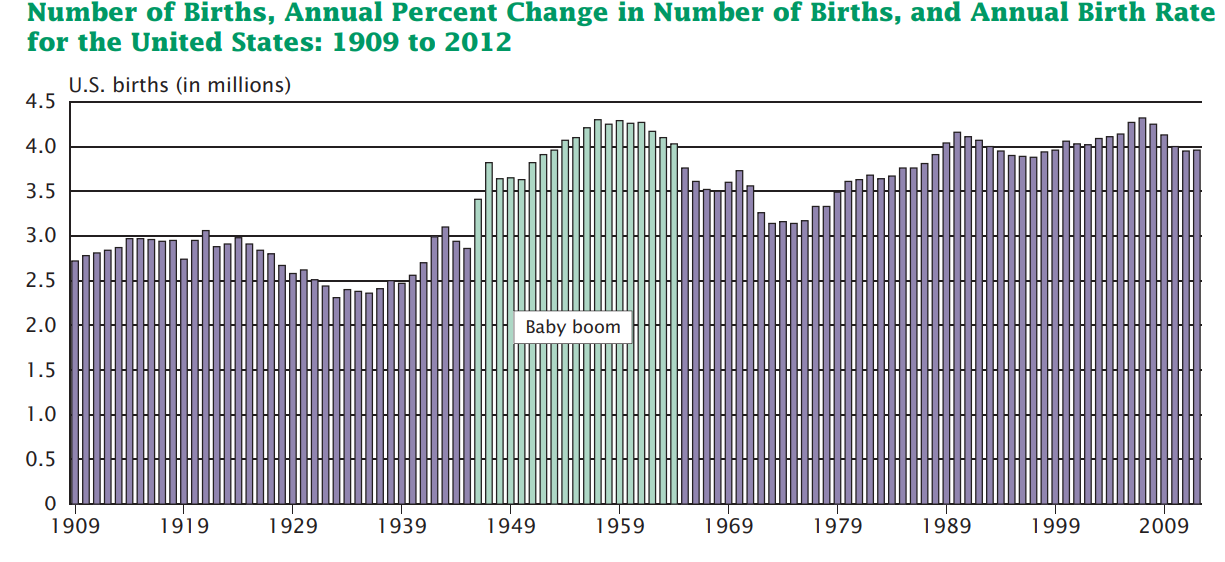

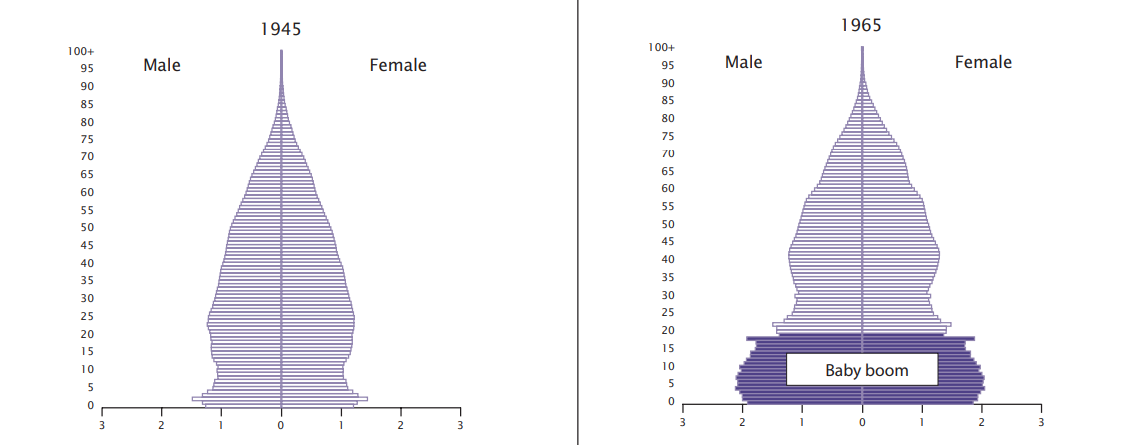

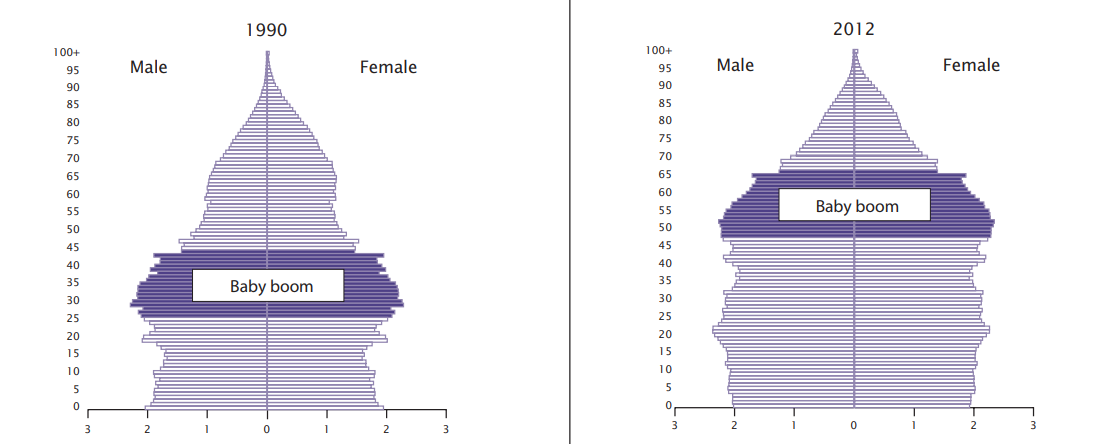

Baby Boom

Naturally, the baby boom is the driving force behind such remarkable retail growth.

The baby boom era was roughly 1947 - 1964, with births peaking in 1957.

Increasing new births would eventually transition into retail customers. And, the retailers can grow alongside the new generation offering things like toy products to home improvement as the generation ages.

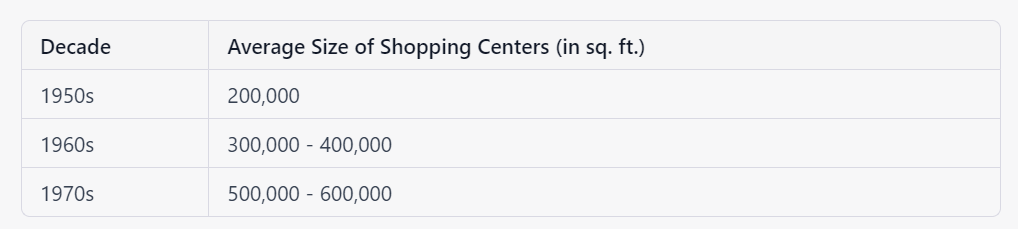

Growth of Malls

Mall development is another factor shaping retail at the time. The U.S. added 8,000 malls during the decade. Additionally, gross leasable area (GLA) increased from 4.6bn square feet in 1960 to 7.9bn square feet in 1970, representing a 72% increase. Malls and large shopping centers played a pivotal role in the expansion of retail space, reshaping how consumers interact with brands.

Not only did the number of malls increase, but the size of each one also grew.

Other Key Characteristics of the 1960s Market

In the 80s, mall outings were a family activity. The parents and kids would split up and meet in the food court for lunch. Each shopper would stop at an average of 7 stores per mall trip. Now, the consumer landscape is vastly different. Consumers are more destination shoppers, stopping at an average of 1.3 stores per trip to the mall. They are in and out of the mall in 76 minutes.

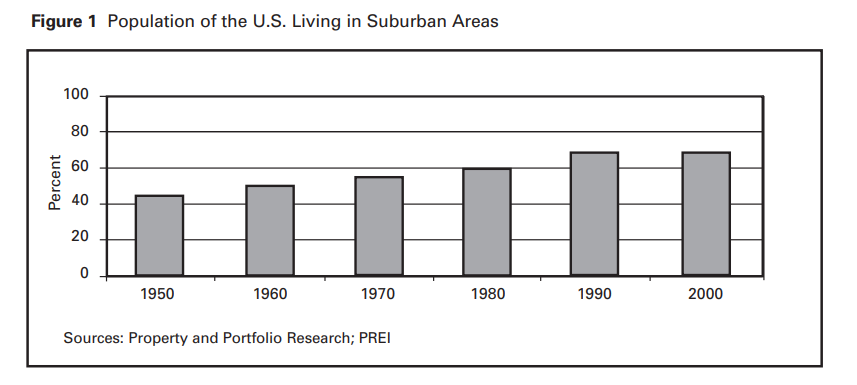

Suburbs - By 1950, roughly 45 percent of the population lived in the suburbs although retail had yet to expand from downtown to the suburbs.

Retail expansion to the suburbs came in 3 phases -

retailers met demand by providing necessities including groceries and everyday items, largely in small formats

scaled-down versions of downtown stores to meet more consumer demand

full-scale suburban shopping experience via malls and shopping centers

Another startling statistic highlighting how retail followed consumers to the suburbs:

1950: 650,000 suburbanites per shopping center

1960: 22,200 per center

1970: 10,000 per center

1990: 4,600 per center

Supply/demand did not reach a balance until the 90s. So, to be successful, you largely had to meet suburban demand / compete on convenience. Afterwards, retailers realized they would soon need to compete on quality and other components to continue their long history of success.

Another interesting point to note is the difference between neighborhood or community centers from malls. The former are often anchored by supermarkets and focus on providing convenient access to everyday items at low overhead costs. On the other side, malls are anchored by departments stores, stand-alone department stores, and stand-alone discount stores, all focused on drawing households from an extended radius to a fulsome shopping experience.

As retail expanded, three models emerged:

Traditional Merchant

The Discounter

Big Box

Before the saturation that occurred in the 90s, the traditional merchant dominated suburban retail by selling quality goods at a substantial mark-up to wholesale. With this success, shopping centers developed around the merchant’s brand to attract traffic to the center with the recognition of the anchor. Developers often valued these anchors so much that they were loss-leaders from a leasing perspective.

Discounters sold lower quality items at lower prices than the traditional retailers. They anchored smaller malls and too were loss leaders (to less of an extent).

Lastly, big box entails warehouse-like structures offering goods comparable to the quality found in traditional retailers but at lower prices.

Let’s look at a pricing example across the three categories.

Department store’s wholesale price for a product is $100. Assume a 50% mark up… the price tag will be $150.

The discounter will sell a lower-quality product. Wholesale may be $80 and with a 50% markup, the items retails for $120.

Big box, offering the same quality product as the department store, squeezes the wholesaler to get the item for $90 wholesale. Apply a 30% markup and the product retails for $117.

As a consumer, where do you shop? Hence the growth in big box since the 80s (Walmart, Target, Kmart).

To put it differently, the big box approach squeezes costs from every part of the supply chain and passes the savings on to consumers. They can do this through purchasing scale economies and tightly controlled overhead. So, a key differentiator seems to be the low cost operator who can pass savings to the consumer.

Overall, the book provides an interesting view into the retail landscape largely from a demographic/macro perspective. It provides great context to all of the negative news we see today around struggling retailers.

Other Takeaways from The Retail Revival

Don’t be a brand stuck in the middle

Consumer preferences are now a barbell. They will shop for value in the morning and a Mercedes in the evening

Sears was in the middle… a mid-market store catering to middle income consumers selling average products… they were stuck in middle purgatory

Be value or be premium/luxury

After the Great Financial Crisis, brands waited for a comeback and refused to accept the new environment. They must learn that the dynamics of the prevailing 50 years have changed and may never come back

In the 1980s, power shifted to the retailers from the brands/vendors

Retailers squeezed them on terms and cost

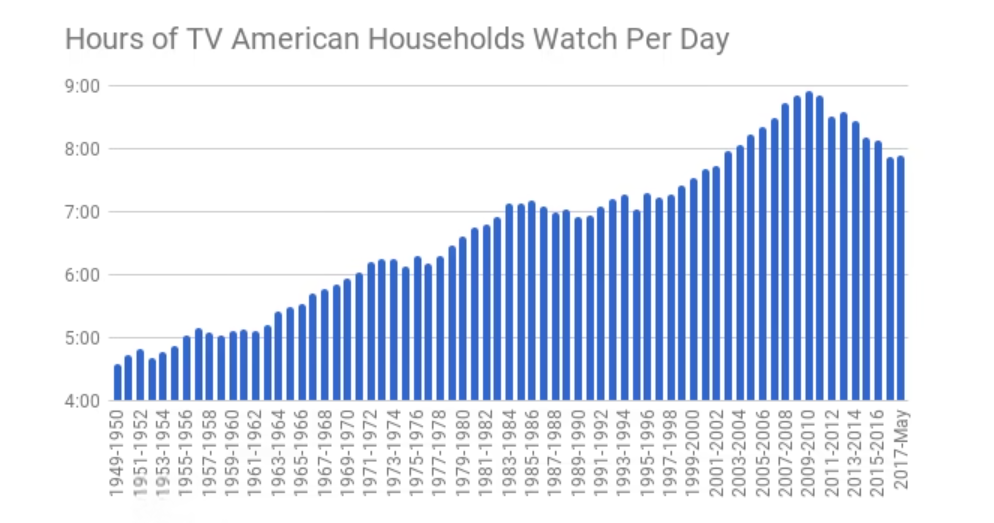

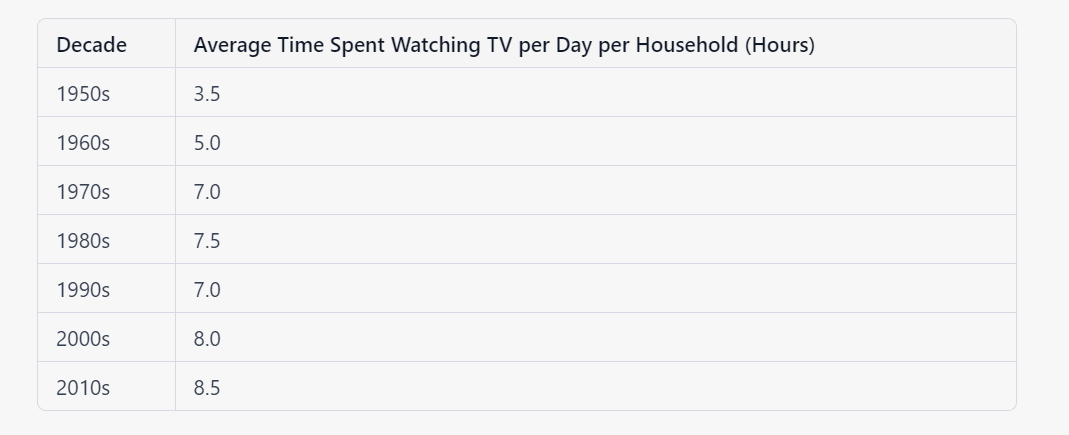

Mass media - TV media let brands reach 80% of consumers through 3 ads during prime time

Number of Americans owning TVs skyrockets

Time spent watching TV also increased!

Back to the Naval post, this is mass-media leverage:

A different source, ChatGPT -

Consumer experience is the sum product of all internal decisions the brand makes

Sam Zell

This is a great interview with Sam Zell.

Take risks and minimize downside. Be right 70% of the time and diligently control downside on the 30%

“The best deals are the deals where the negotiators have reached the point of indifference, where they would take either side of the transaction”

Sam is a consumer of capital. He will always go back to the capital trough… so best to make sure his partners are happy in negotiation outcomes

Buy a ticket - you can’t win if you aren’t in the game. Sam is a professional opportunist and buys tickets for a living

++

Until next time.

John Galt