10. Credit Agreement Magic (Part 2/2)

10. Credit Agreement Magic (Part 2/2)

Loan Docs, J. Crew and Neiman Marcus

Let’s continue exploring debt docs by honing in on credit agreements. We will focus on those governing term loan and cash flow revolver facilities - excluding asset-backed-loans (ABLs) as they tend to be slightly different.

I suggest starting with this post on HY indentures that defines many overlapping terms found in credit agreements (CA).

Before we jump in, a quick reminder - while the information may be difficult to read, it’s important to have a foundational understanding of debt docs as an owner of assets with debt financing. You can create equity value by prudently navigating the credit ecosystem. My goal here is to provide a basic understanding of debt docs and then show how you can structure/use these facilities to your advantage (as an owner or issuer).

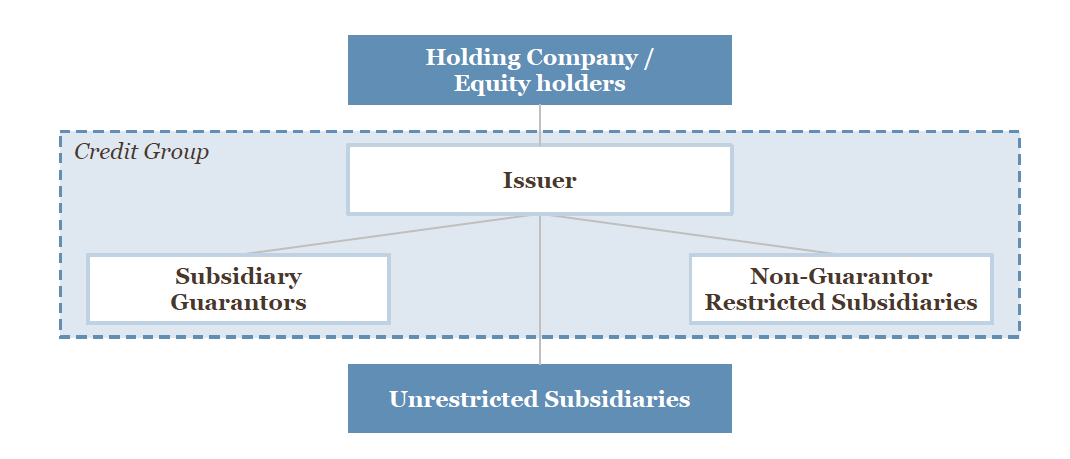

Restricted and Unrestricted Subsidiaries and Loan Parties

Our prior discussion noted that indentures often grant the borrower unlimited investment capacity between the issuer and its restricted subsidiaries regardless of whether those subs guarantee the high yield debt.

In other words, high yield covenants are flexible in permitting actions between and among the issuer and its restricted subsidiaries.

On the other hand, credit agreement covenants have historically been more focused on leakage from the borrow and/or guarantors (referred to as the loan party) to non-guarantor subsidiaries.

So, credit agreements often allow unlimited investments between and among loan parties, but they limit investments by loan parties in non-loan party restricted subsidiaries.

This is an important point. Non-guarantors are considered to be a non-loan party entity. And, the CA restricts investments between the loan party and non-loan party subs (or, between guarantors and non-guarantors).

While indenture and credit agreement information seems dry, we are setting up the discussion for a more interesting look at how issuers have been creative in moving value outside of the credit group. For instance, J. Crew, a famous case that we will review below, moved valuable collateral (IP) from loan parties to unrestricted subsidiaries. Therefore, the value / IP is now beyond the reach of lenders. Issuers can also designate restricted subsidiaries that own valuable assets as unrestricted subs.

So, we will look at 1) how issuers can move value outside the credit group and 2) how issuers can reclassify a restricted sub as an unrestricted sub. Both points accomplish the goal of moving value outside of the lender’s reach.

Limitations on Investments, Restricted Payments and Restricted Debt Payments

Indentures often have just one covenant restricting an issuers ability to move assets out of the credit box - the restricted payment (RP) covenant.

Credit agreements often divide this limitation into three covenants:

limitations on investments

limitations on prepaying subordinated debt

limitations on paying dividends and other distributions and redeeming or repurchasing the borrower’s capital stock (restricted payments)

Incremental Facilities and Incremental Equivalent Debt

A credit agreement typically allows the issuer to increase the debt quantum (through revolver borrowings or additional term loan issuance) under the incremental facilities clause.

Typically, incremental facilities are permitted in an amount equal to the sum of:

fixed dollar amount equal to a percentage of the borrower’s EBITDA at closing (more aggressive deals will have an EBITDA grower… which naturally increases the amount of incremental capacity as EBITDA expands)

100% of voluntary prepayments of term loans or other pari passu debt plus 100% of commitment reductions on the revolver

additional pari passu debt so long as the pro forma first lien leverage does not exceed first lien leverage at closing

There are more nuances here, interesting nonetheless, but beyond the ultimate purpose of our discussion. We can always come back to this.

Essentially, the purpose of the incremental terms are to govern how much incremental debt the issuer can obtain after closing and which thresholds need to be met in order to assume incremental facilities.

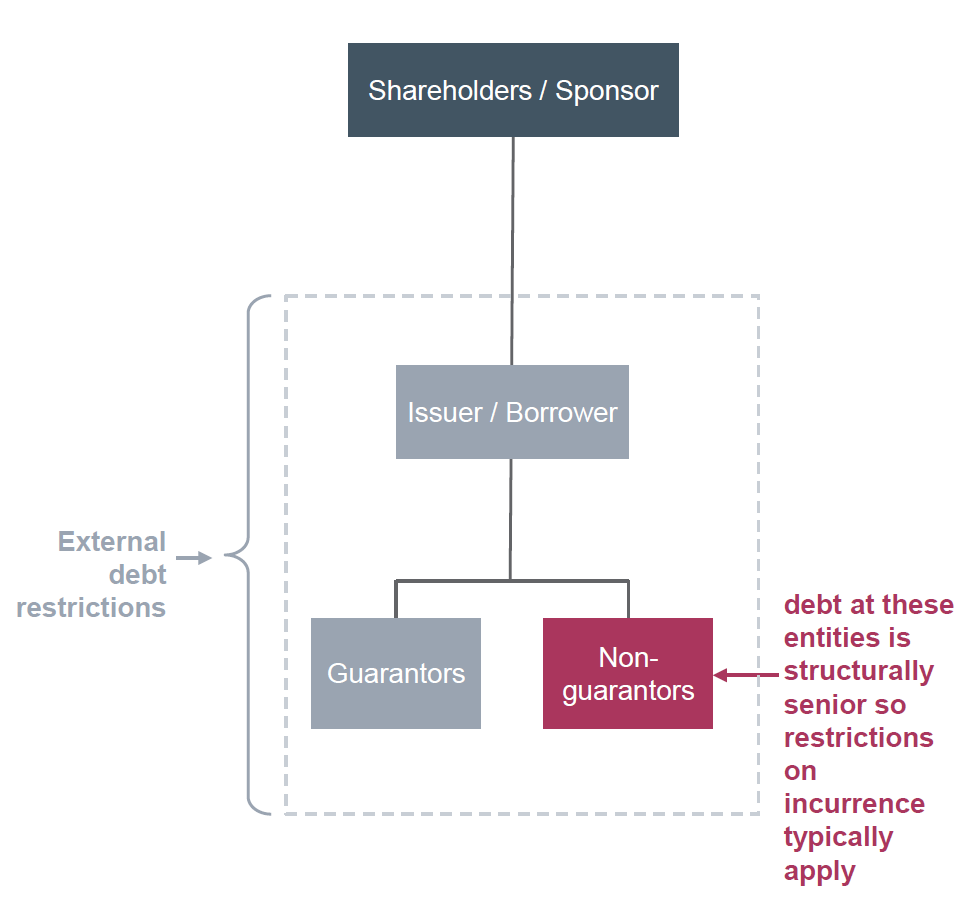

Ratio Debt

Indentures often tie ratio debt to fixed charge coverage ratios (FCCR) whereas credit agreements treat ratio debt more similar to incremental, measuring against specified leverage ratios and, if applicable, interest coverage ratios.

The main difference between the incremental and ratio exception is that the incremental can typically only be incurred by the borrower while ratio debt can be incurred by the borrower or any of its restricted subsidiaries.

Importantly, since any debt incurred by a subsidiary that is a non-guarantor is structurally senior to the credit agreement debt, there is usually a cap on how much debt non-guarantor subs may incur utilizing this basket!

Finally, that’s the end of walking through important terms in debt docs. Now we can turn to the fun stuff - let’s see how this works in practice. The creative side of leveraged finance.

Leveraged Finance Key Concepts

Remember, this is the anatomy of an LBO with debt financing.

As mentioned above, there is usually a cap on debt incurred by non-guarantors as this is structurally senior to the credit agreement debt. Here is the illustration:

And restricted debt payments exist to limit transactions that allow value to leave the restricted group to pay other creditors. This concept limits the issuer from repaying or redeeming debt that is contractually subordinated to the credit agreement debt. Illustrated below -

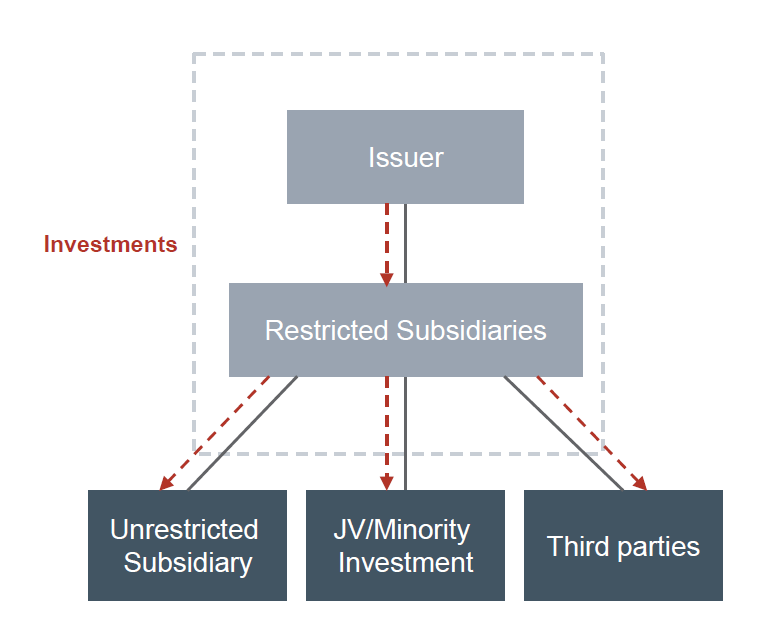

Lastly, the investment covenant from the previous post - this limits investments in entities outside of the restricted group including acquisitions, intercompany debt obligations and investments in JVs/minority equity positions.

Illustrated here -

Case Studies - The Fun Part

Here’s an overview of restricted payments and investments covenants -

There are many clauses within credit agreements that define the access and usage conditions of, say, the builder basket. We’ll keep this high level for now and focus on the concepts.

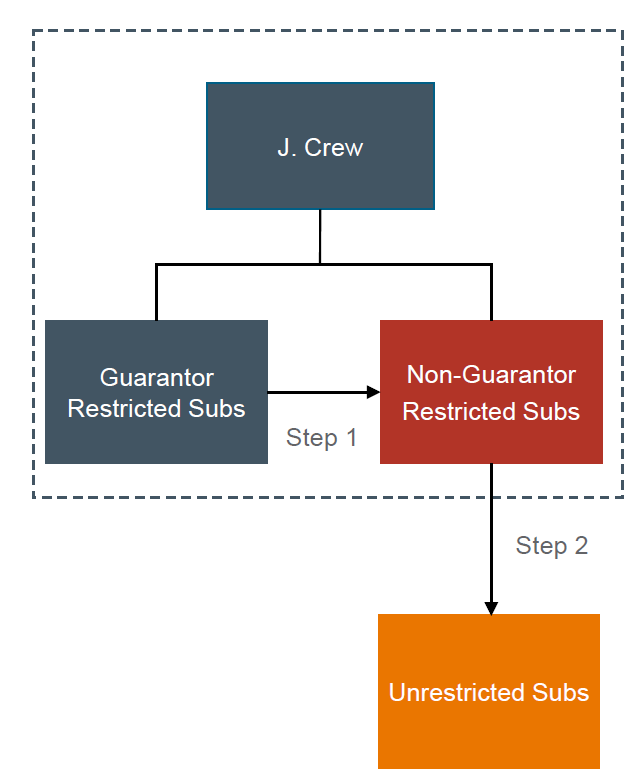

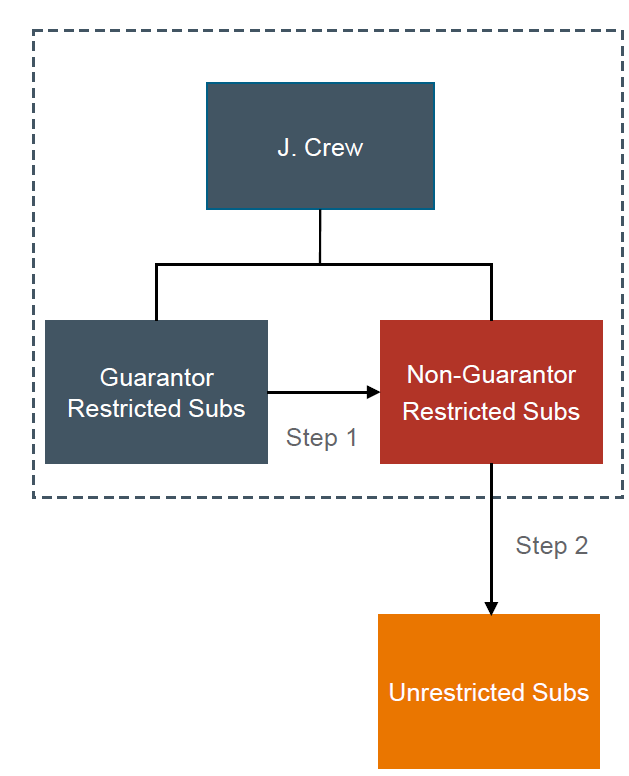

J. Crew - Trap Door Investments Provision

J. Crew moved valuable intellectual property out of the restricted group through a two step process:

*It’s helpful to reference the picture below after each sentence to follow what’s happening*

A guarantor restricted sub used an investment basket to contribute valuable trademarks to a non-guarantor restricted sub

Remember, non-guarantor assets are still subject to the covenants but is now outside of the loan party

The non-guarantor restricted sub relied on a separate investment basket that allowed it to make an investment into an unrestricted subsidiary

J. Crew then refinanced earlier maturing debt at the unrestricted subsidiary, now secured by the transferred IP!

Takeaway: 1) assets were moved outside the credit group and covenant purview and 2) newly free assets used to secure other debt at the unrestricted sub level

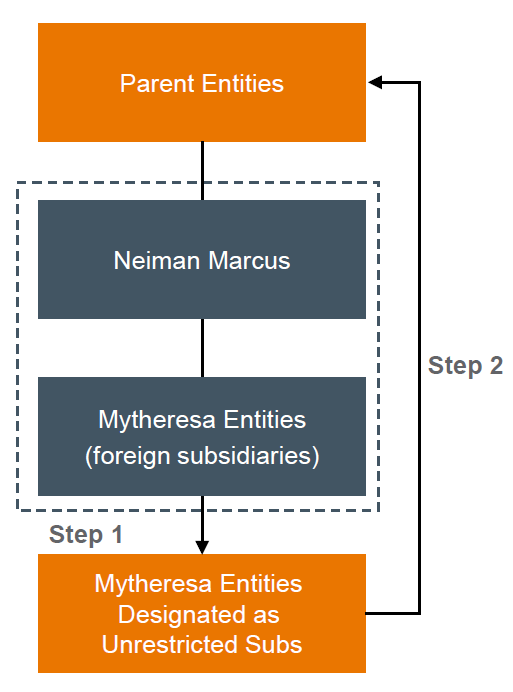

Neiman Marcus’ Unrestricted Distribution Through Designation

Neiman Marcus transferred Mytheresa, a high growth business, to its shareholders via a 2 step process.

Designation of Mytheresa as an unrestricted subsidiary

NM used RP and investment capacity (through the builder basket and other capacity) to designate Mytheresa as an unrestricted sub

Once designated, the assets no longer provide credit support or subject to covenants and any pledge of equity is released

Dividend of stock to the parent entities

Transfer ownership of Mytheresa via a stock dividend to Neiman Marcus shareholders

Use the RP basket that permits unlimited distributions of equity interests in unrestricted subs

Takeaway: spin out the valuable, high-growth business by converting unrestricted sub investment capacity to RP capacity

So, going back to this main anatomy picture, we an see how a creative understanding and use of debt docs allows the issuer / private equity owners to carve value out of the confines of the credit group.

We’ll leave our discussion on debt docs here for now. It can feel boring learning about leveraged finance concepts, but hopefully you see how an understanding of debt docs can lead to immense value creation at the sponsor level.

You don’t need to be an expert in these concepts by any means. But, with a basic understanding, you will know which questions to ask and what goal to solve for… and that was my intention with this two part series.

++

Until next time.

John Galt